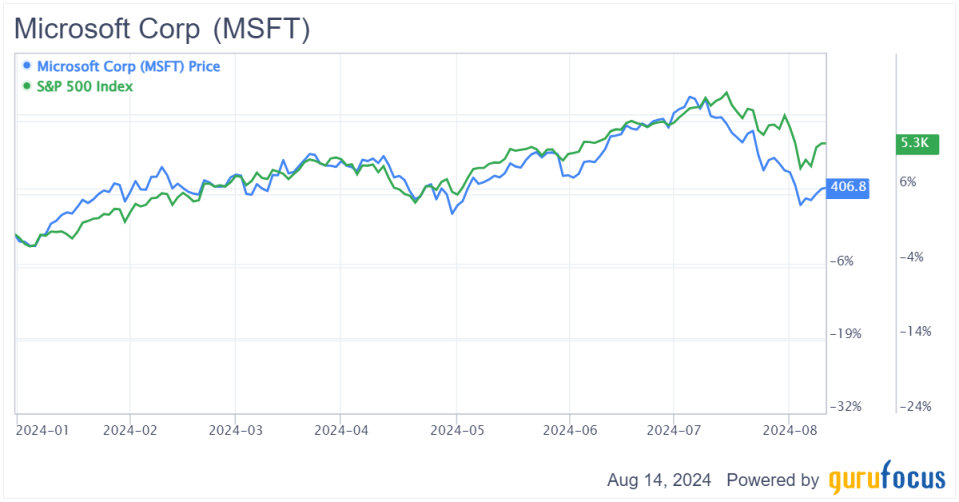

Despite being seen as a key beneficiary of the artificial intelligence boom, primarily due to its strategic investment in OpenAI, Microsoft Corp.’s (NASDAQ:MSFT) stock has underperformed broader markets and its mega-cap peers this year. After a strong start, the stock has only gained about 7.10% year to date. This is a significant decline from its mid-July peak, where it was up nearly 25%.

The downturn can be attributed to weaker-than-expected near-term prospects at Azure following the latest earnings release and the broader global market sell-off driven by disappointing employment data, which heightened recessionary fears.

Even with this moderate sell-off, despite strong fourth-quarter earnings, I believe there is no reason to be less bullish on Microsoft now than a few months ago. The company’s core fundamentals remain robust, with all three business segments continuing to show solid growth, led by the impressive performance of the Intelligent Cloud division. Microsoft’s operating leverage remains resilient, and the company continues to be a free cash flow powerhouse, even as it ramps up research and development and capital expenditures. I see a clear path to double-digit forward returns, making Microsoft a compelling long-term opportunity.

I have long held the view that Microsoft would be a frontrunner in the AI revolution, and the past year has only strengthened this belief. The company’s operational momentum continues to build, reinforcing my confidence. Despite the market’s overreaction to fourth-quarter 2024 earnings, I believe Microsoft still has significant growth potential. For investors who buy at current levels, this could be an excellent opportunity to secure substantial future gains. In this analysis, I will explain why I remain bullish on Microsoft and why I believe the market’s response to the recent earnings report was unwarranted.

Continued growth in Azure and cloud services

Despite the expected deceleration in Azure’s growth through the first half of fiscal 2025, Microsoft has witnessed substantial growth in recent quarters. Azure Cloud Services reported a 29% revenue increase in the fourth quarter, while Microsoft Cloud recorded a 21% rise, driven by the broader adoption of AI-enhanced services across its offerings. In recent times, the performance of Microsoft’s quarters has largely hinged on Azure’s success, and the fourth quarter was no exception. However, it is important to note the slowdown in Azure’s growth was primarily due to AI-related capacity constraintsindicating a supply issue rather than a lack of demand. Demand for Azure AI remains robust, underscoring its pivotal role in driving the company’s growth.

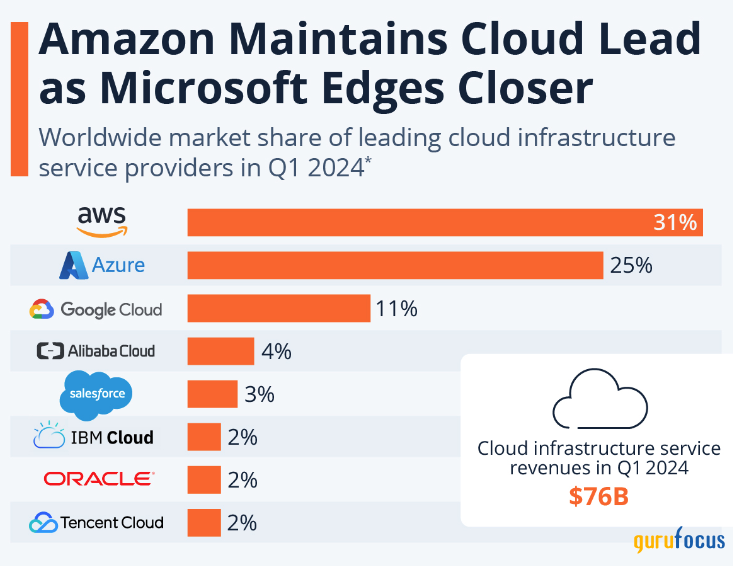

Microsoft, a significant client of Nvidia Corp. (NASDAQ:NVDA), is in fierce competition with Alphabet’s (NASDAQ:GOOG) Google and Amazon (NASDAQ:AMZN) within the cloud market. As of the first quarter of 2024, the company’s share of the global cloud market grew from 22% to 25% over the prior four quarters, outpacing both Amazon Web Services and Google Cloud Platform. While AWS has long been the leader in cloud computing, the competitive landscape is shifting. Recent developments suggest Azure could potentially overtake AWS as the leading cloud service provider by 2026. The Azure OpenAI service, which enables customers to build AI applications without the need for expensive hardware, is a critical driver of this growth. As Microsoft’s AI and cloud services continue to evolve, the company is well-positioned to challenge AWS’s dominance in the coming years.

Source: Statista

Microsoft’s aggressive investment in AI for Azure is attracting new customers and even luring AWS and GCP users to switch. The increasing revenue and profits generated from AI demonstrate the company’s strategy is moving in the right direction, albeit at a steady pace rather than explosive growth. The current supply constraints highlight the overwhelming demand, justifying Microsoft’s continued investment in AI. The company has outlined plans to invest billions in data centers and AI hubs globally, including a multibillion-dollar investment in Spain. Additionally, it has partnered with Lumen Technologies (NYSE:LUMN) to expand network capacity and support the rising demand on data centers.

This aggressive investment in AI infrastructure underscores management’s strong conviction in capturing a share of the potential $1.30 trillion market opportunity. Microsoft’s broad representation in the cloud value chain positions it well to anticipate and meet demand, making its continued investment in data center expansion a logical and necessary step.

Strong fourth-quarter financial performance despite market overreaction

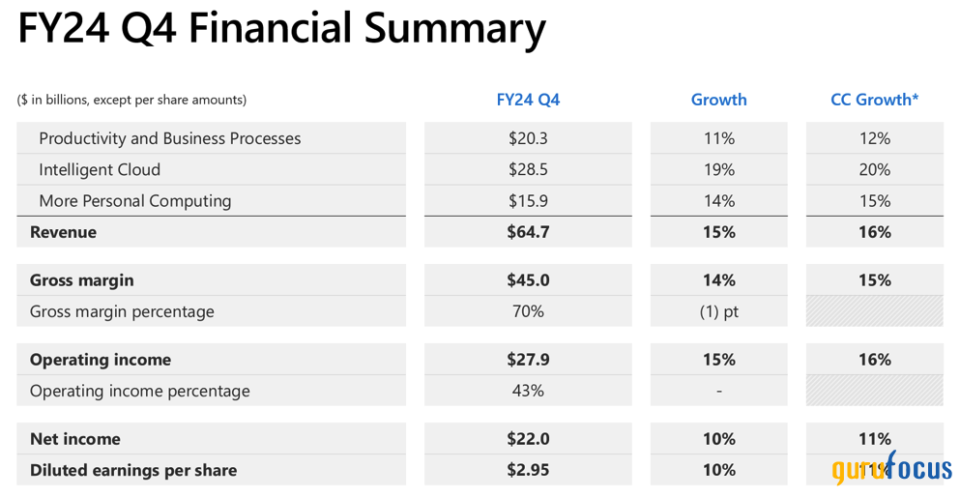

The software giant delivered another robust quarter on July 30, surpassing revenue and earnings per share consensus estimates. The fourth quarter saw a 15.20% year-over-year increase in revenue, with adjusted earnings rising from $2.69 to $2.95 per share, driven in part by strong operating leverage. Notably, Microsoft Cloud posted 21% year-over-year growth, while Azure and Cloud Services recorded a 29% increase. Of the latter, 8% was driven by Microsoft’s generative AI services, which, while contributing modestly, still reflects the significant impact of AI on Microsoft’s largest growth segments. Contrary to market expectations for explosive growth, I view the current levels of growth as reasonable and on the right trajectory, likely to accelerate as Microsoft’s substantial AI investments begin to pay off.

Source: Microsoft’s Investor Relations

Investors were disappointed by what they perceived as a slowdown in Azure’s growth, which reported a 29% year-over-year increase (30% in constant currency), falling short of both the company’s forecast of 30% to 31% and analysts’ expectations of over 30%. However, I find it hard to label a 29% growth rate as a “slowdown.” The market’s reaction, leading to a sell-off, seems irrational to me. Microsoft is not overbuilding; it is expanding its capacity to meet customer demand. As this capacity comes online through continued investments, I expect growth rates to pick up.

Balancing AI investments with financial health

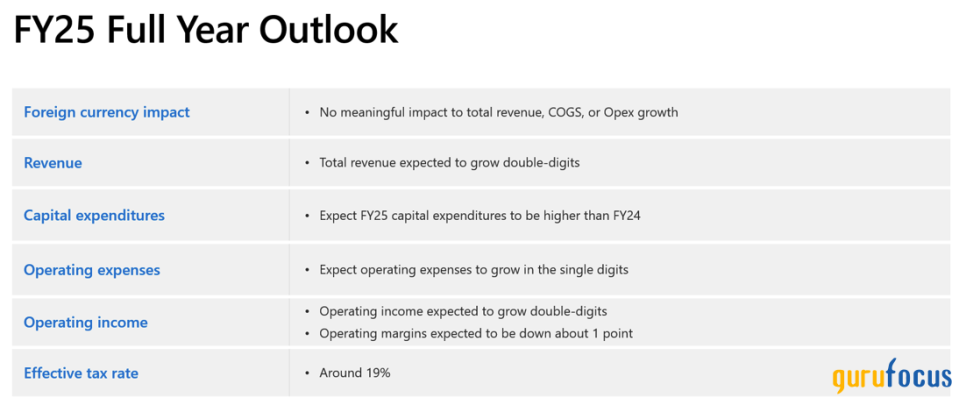

The transition to generative artificial intelligence at Microsoft is resource-intensive, with capital expenditures in fiscal 2024 reaching $45 billion and even higher expenditures for 2025, according to management forecasts. This has raised concerns about the company’s profit margins moving forward. While Microsoft projects double-digit revenue and operating income growth, the increased capex will inevitably impact profitability. Investors should not expect significant margin expansion in the near term as operating margins are expected to hold steady with a slight decline of about 1%. However, in the longer term, as AI infrastructure investments stabilize and mature, I anticipate significant upward pressure on operating margins given the potential of AGI to drive widespread benefits.

Source: Microsoft’s Investor Relations

Microsoft’s strong free cash flow generation is a testament to its solid operating leverage. The company generated $12.40 billion in levered FCF during the quarter, despite a $5 billion year-over-year increase in capex. This robust FCF has further strengthened its balance sheet, which now boasts a $75 billion cash reserve.

This financial flexibility positions Microsoft well for significant acquisitions, as evidenced by the $69 billion Activision Blizzard deal in 2023. Capex as a percentage of total revenue has surged from the low teens to the high teens, driven by the generative AI boom since 2023. Management has indicated that capex investments will increase materially in 2025, surpassing 2024 levels. While this elevated spending might create a near-term headwind on FCF, the strong demand outlook, supported by cloud migrations and AI adoption, justifies this strategic investment.

Valuation perspective

Following the recent sell-off, Microsoft is trading at 21.50 times forward earnings, positioning it as an attractive pick among the Magnificent Seven. This valuation is slightly lower than Amazon’s price-earnings ratio of 23 and Apple’s ratio of 25, making Microsoft a compelling option, particularly since only Meta is trading at a cheaper valuation. I anticipate Microsoft maintaining a 25 to 30 times earnings multiple as its top-line growth moderates to the 6% to 8% range.

This outlook is underpinned by the company’s strong net cash position, highly recurring revenue base and projected long-term net margins of 40% to 45%. Investors can expect returns driven by both top-line growth and earnings yield, with the added confidence that Microsoft has historically been a reliable buy during market pullbacks. Given the current market meltdown in the U.S. due to recessionary fears, now appears to be an ideal time to invest in a high-quality company at a reasonable price. Microsoft’s strong financial performance across cycles further enhances its attractive return proposition.

Source: valueinvesting.io

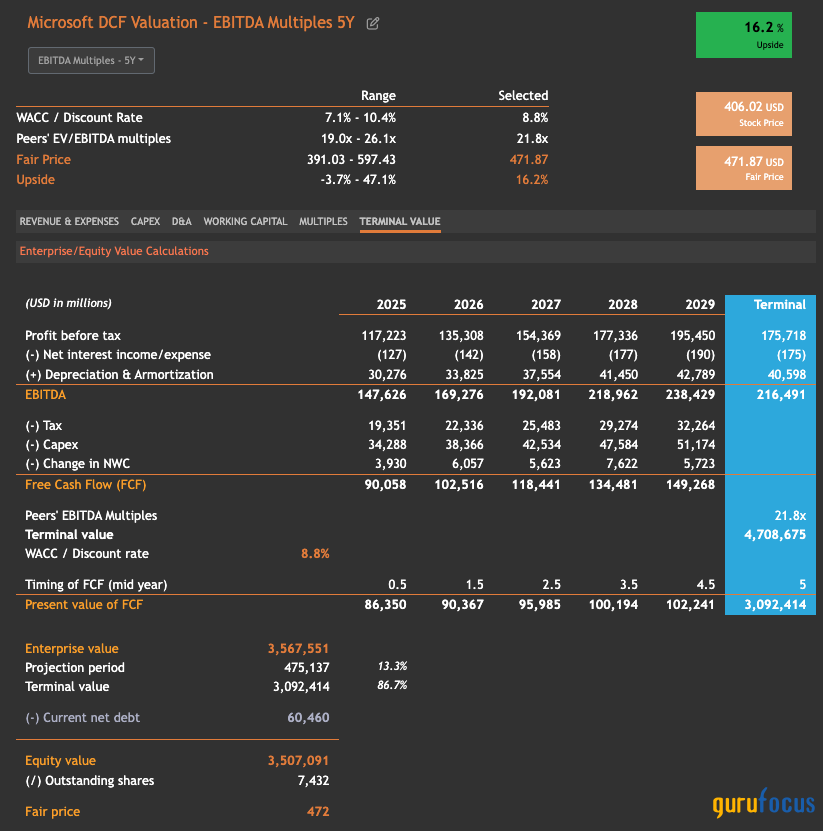

From a discounted cash flow perspective, using a discount rate of 8.80% and a five-year exit Ebitda multiple of 21.80, aligned with peers, I derive a valuation of approximately $472 per share. This suggests an upside of 16.20% based on conservative estimates. This valuation reflects my belief that Microsoft is likely to maintain stability at current levels as management continues to execute on its AI roadmap.

Considering Microsoft’s significant growth potential amid the AI boom, its integration of AI technology and continued increases in revenue and earnings, this valuation provides a substantial margin of safety. Additionally, the company’s potential to expand and enhance revenue streams in emerging and developing markets is strong. The company is well-positioned to gain market share from AWS and GCP, particularly with its ongoing advancements in AI through its dedicated AI division. These initiatives are expected to further strengthen Microsoft’s position in the tech industry, driving sustained growth and value creation for shareholders.

Wrapping up

Despite recent market overreactions and a temporary slowdown in Azure’s growth, Microsoft’s core fundamentals and strategic investments in AI underscore its long-term potential. The company remains a solid investment opportunity, especially in a volatile market, with strong financial performance and a well-positioned AI roadmap likely to drive future growth and value creation for shareholders.

This article first appeared on GuruFocus.

{kind=link}