While Asian currencies have been on a modest decline since Middle East tensions flared up, Japanese financial giant MUFG Bank Ltd. said the Philippine peso was the biggest loser among regional currencies, given the domestic economy’s high exposure to imported oil.

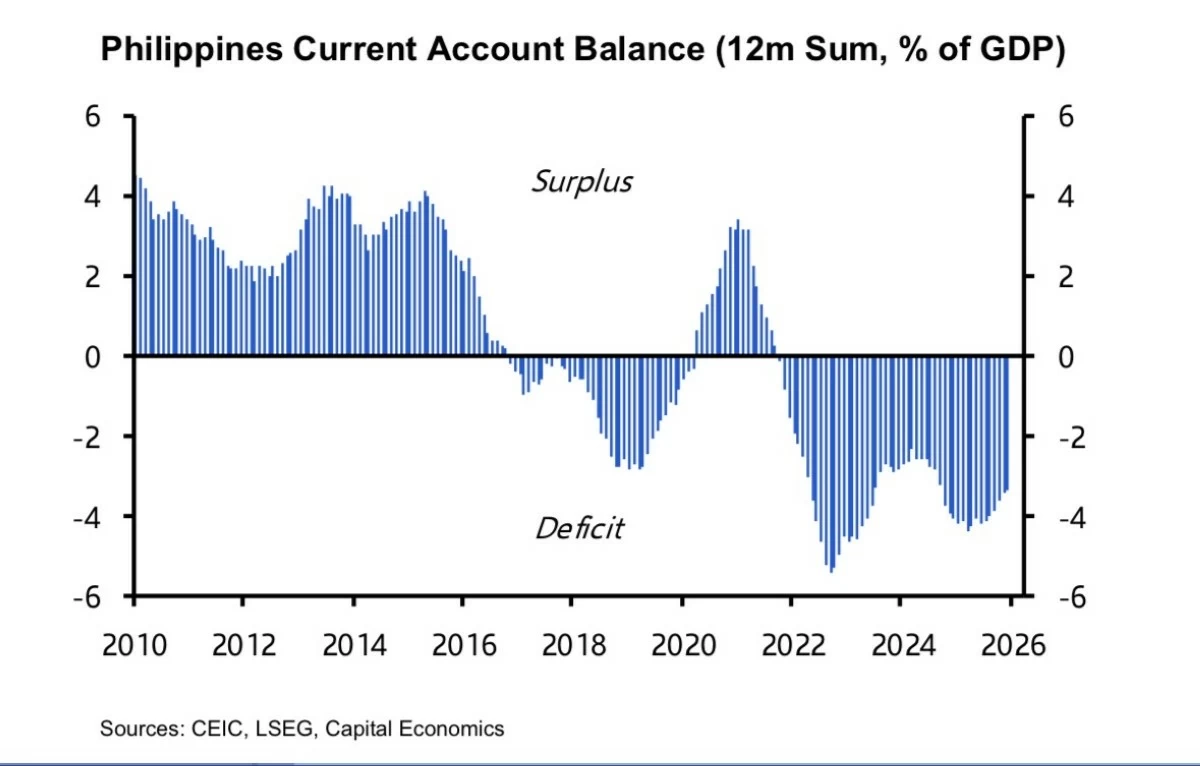

Separately, think tank Capital Economics said the global oil price spike would widen the Philippines’ current account deficit, putting more pressure on the local currency.

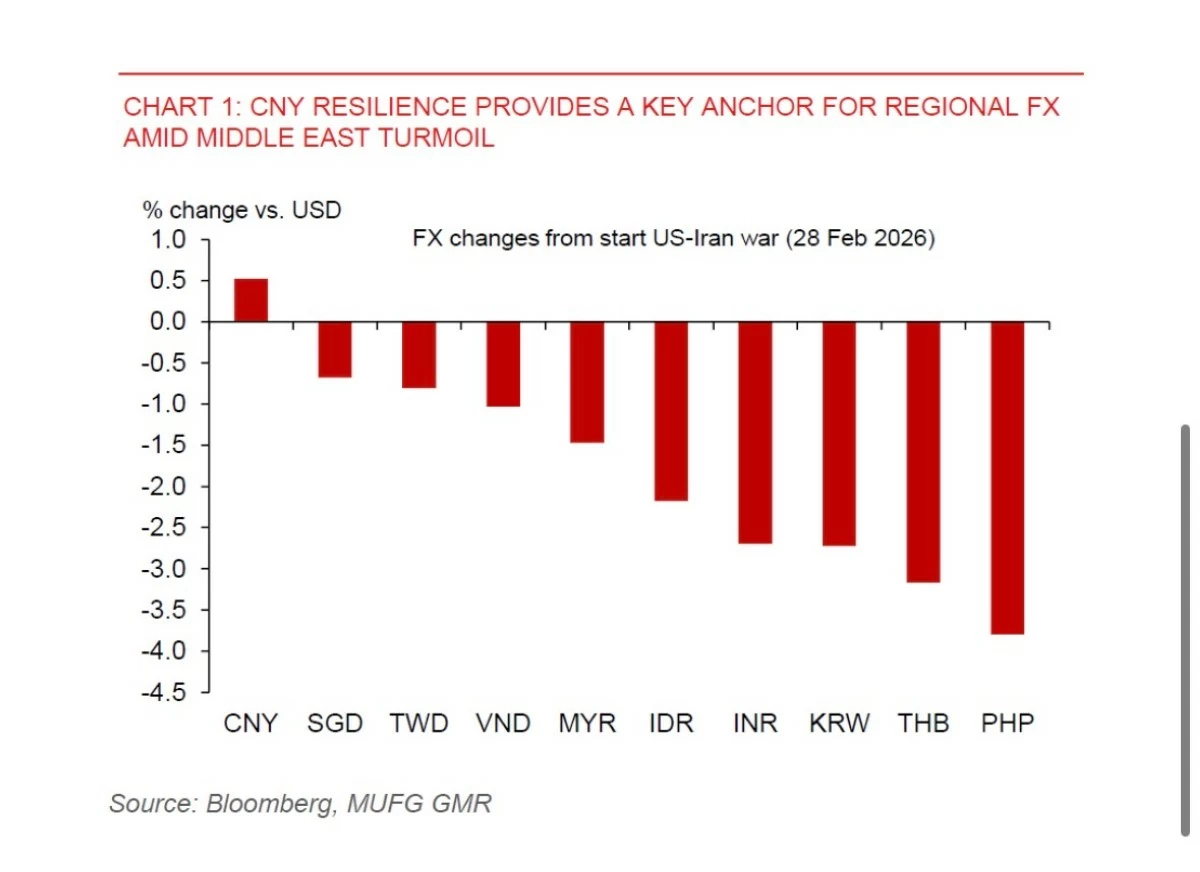

In a report on Wednesday, April 22, MUFG Global Markets Research data showed that the peso has declined by nearly four percent against the United States (US) dollar since the onset of the US-Iran conflict in late February. This sharp depreciation has brought the currency to the ₱60-per-greenback level as of Wednesday midday.

Screenshot

Last month, the peso plunged to record-low levels, nearing the ₱61:$1 threshold.

“The peso is vulnerable given its heavy reliance on Middle Eastern crude imports,” MUFG senior currency analyst Lloyd Chan said, underscoring the local currency’s stress point as energy costs remain under pressure.

With Brent crude for June delivery hovering near $100 a barrel, the Philippine economy faces higher costs for essential energy imports.

This trend is mirrored by the Thai baht, which recorded the second-largest decline among regional currencies at over three percent, as Thailand runs the “largest oil and gas trade deficit in the region.”

Tensions from the “prolonged standoff” are now weighing heavily on investor sentiment. A second round of talks failed to materialize after Iran rejected further peace discussions, and while the US extended a ceasefire timeline, the initial two-week truce is expected to expire on April 22.

Meanwhile, the US continues to blockade Iranian ports to halt oil shipments, a move intended to pressure Tehran into a deal but one that risks further military escalation.

While the peso grapples, the Chinese yuan has acted as a “key anchor” for the region, appreciating by roughly half a percent against the US dollar during the same period.

Other resilient performers include the Singapore dollar and New Taiwan dollar, both of which saw declines of less than one percent.

Even with the peso’s weakness, Chan noted that “the overall decline in Asian foreign exchange (forex) has so far been relatively modest compared to the sharp dislocations seen during the Russia-Ukraine conflict.”

In an April 21 report, Capital Economics senior Asia economist Gareth Leather and deputy chief emerging markets (EMs) economist Jason Tuvey said that in the Philippines, “higher energy prices will cause the current account deficit, which had started to improve late last year, to widen again.”

Screenshot

The think tank noted that the Philippine peso has already faced fresh downward pressure since the war broke out.

Screenshot

A wider current account deficit—when a country imports more goods, services, and capital than it exports—increases demand for foreign currency over the peso, putting downward pressure on the local currency’s value.

While the government has declared a state of national energy emergency and moved to curb fuel consumption, Capital Economics warned that the spike in domestic oil prices is expected to dampen demand.

Capital Economics estimates showed that the Philippines’ net energy imports are equivalent to over four percent of gross domestic product (GDP).

“Most countries in Asia are big net energy importers, and the crisis in the Middle East will deliver a stagflationary shock to the region,” Capital Economics warned.

Stagflation is an economic condition where slow growth, high unemployment, and rising inflation occur at the same time.

After last year’s sharp slowdown in the aftermath of the flood-control infrastructure corruption scandal, Capital Economics expects Philippine GDP growth to decelerate further to a below-consensus 3.8 percent in 2026, poised to be a new post-pandemic low.

The reduction in Capital Economics’ growth forecast for the Philippines due to the war was among the largest, surpassed only by downgraded projections for Pakistan and the Gulf Cooperation Council (GCC), comprising Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE).

“The early signs suggest that the spillovers from the war are acting as a fresh headwind to economic activity, with the PMIs [purchasing managers’ indices] dropping back in March,” the think tank noted.

Capital Economics also noted that higher fuel prices and a weaker peso pushed headline inflation up to an above-target 4.1 percent year-on-year in March, while core inflation also ticked up.

“The Bangko Sentral ng Pilipinas (BSP) left rates unchanged at an off-cycle meeting in March. As it balances higher inflation against sluggish growth, we expect policy to remain unchanged,” Capital Economics said.

The BSP’s Monetary Board (MB) will decide on the monetary policy stance on Thursday, April 23.

{kind=link}