The company’s long-term prospects are good, but investors should proceed with caution because of its valuation.

If you’ve been keeping up with the tech industry, you’ve witnessed artificial intelligence (AI) go from a niche topic to the hottest theme in business. It’s almost inescapable at this point. Many businesses have benefited from the AI boom, but maybe none more so than Nvidia (NVDA -0.36%).

The chipmaker’s stock is up by more than 160% this year alone, continuing a rally that has seen its stock price increase by more than 760% in the past year and a half. It even briefly took the title of the “world’s most valuable public company,” passing tech titans Microsoft and Apple.

Nvidia’s run has been remarkable, there’s no doubt. However, with so many investors rushing to buy the stock, others are wondering whether the hype has pushed it into bubble territory.

How did Nvidia get to this point?

Nvidia is known for its graphic processing units (GPUs) — blazing-fast parallel processors that are among the best hardware available for providing the computational power necessary to train and deploy AI models. According to some estimates, the company recently held as large as a 95% share of the AI chip market, so to say it’s important to the AI pipeline would be an understatement.

There’s also the data center aspect. Data centers are the foundation of AI infrastructure, providing the computational power needed to process and analyze massive amounts of data. Without that ability, there’s no AI as we know it.

Most of the companies that run these data centers have built them using massive volumes of Nvidia’s GPUs — among them, major cloud platform providers Amazon, Microsoft, and Alphabet. Their unprecedented demand for Nvidia’s AI-related hardware has put the company on a whole new trajectory.

Its earnings from the first quarter were beyond impressive

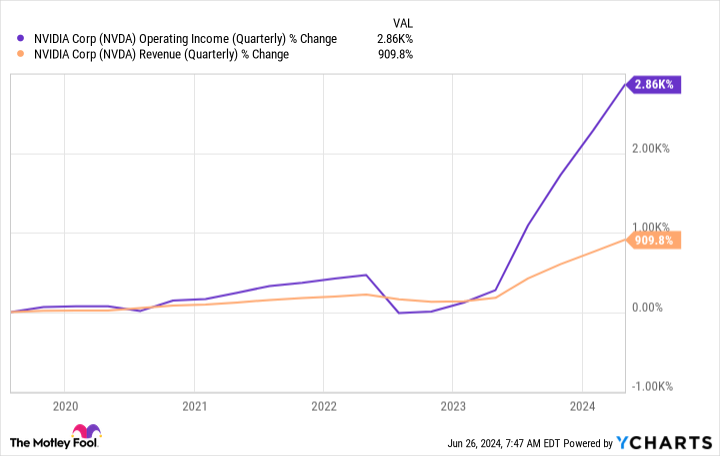

Nvidia’s financials have soared due to the unprecedented demand. In its fiscal 2025 first quarter, which ended April 30, the company reported year-over-year gains that most large companies can only dream about.

Its revenue increased 262% to $26 billion, led by a 427% increase in data center revenue of $22.6 billion (both company records). Arguably more impressive, though, was the 690% jump in operating income to $16.9 billion. And its gross margin went from 64.6% to 78.4% — not too shabby.

NVDA Operating Income (Quarterly) data by YCharts.

Nvidia is surely benefiting from increased demand for its chips, but an underrated upside of being the undisputed leader in the space is the pricing power that comes with it. With demand continuing to outstrip supply, Nvidia should be able to charge premium prices and maintain its impressive margins.

To say the stock is expensive would be an understatement

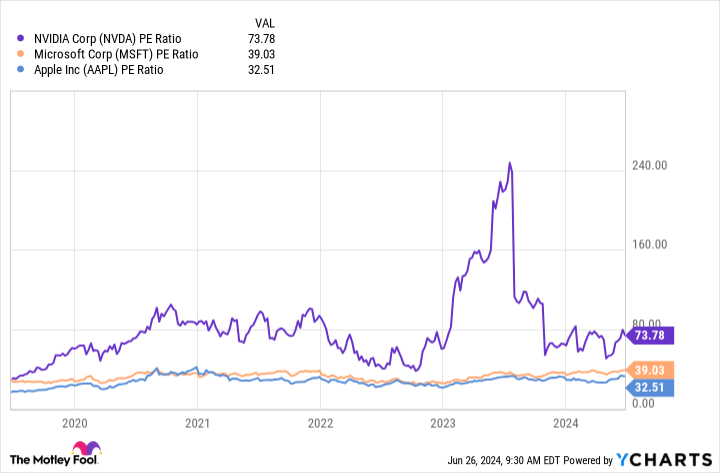

Nvidia’s financials have been impressive, but the stock is one of the most expensive on the market. The surge in earnings has brought its valuation down to a more reasonable level than the roughly 240 price-to-earnings ratio it had last year, but it’s still high. Just look at how it compares to tech giants Microsoft and Apple.

NVDA PE Ratio data by YCharts.

A high valuation can be justified when the company’s growth prospects match it, but at some point, even the most promising companies can reach valuations that go beyond what’s fundamentally reasonable.

In Nvidia’s case, many investors are rushing to buy the stock because of a fear of missing out. This happens with virtually every promising new technology. The problem is that much of the run-up is built on speculation, and with that comes an increased risk of a sharp correction if investors’ expectations aren’t met.

Is Nvidia a great company? Absolutely. But is it fair to say its stock is flirting with bubble territory? I would certainly say yes.

Slow and steady often wins the race

Nobody can reliably predict what the stock market will do in the near term, nor know if Nvidia or the AI sector as a whole are in bubbles destined to pop. You can look to history as an indicator, but nobody can say for certain. That’s why I believe the best approach to Nvidia’s stock now is to dollar-cost average your way into a stake.

When you dollar-cost average, you decide on a specific amount you can commit to investing and then set a regular schedule to make those investments. For example, you might commit to investing $400 monthly into Nvidia. From there, it’s up to you to decide if you want to divide the investments into four $100 weekly investments, two $200 bi-weekly investments, or whatever works best for you. Sticking to your schedule is more important than whatever frequency you choose.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Stefon Walters has positions in Apple and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

{kind=link}