Shake Shack may finally be positioning itself for stronger share price returns.

On Aug. 1, popular burger chain Shake Shack (SHAK -1.94%) reported financial results for its fiscal second quarter, showing revenue growth of 16%. That was almost as good as the 18% revenue growth Chipotle Mexican Grill (CMG -2.78%) reported in its second quarter.

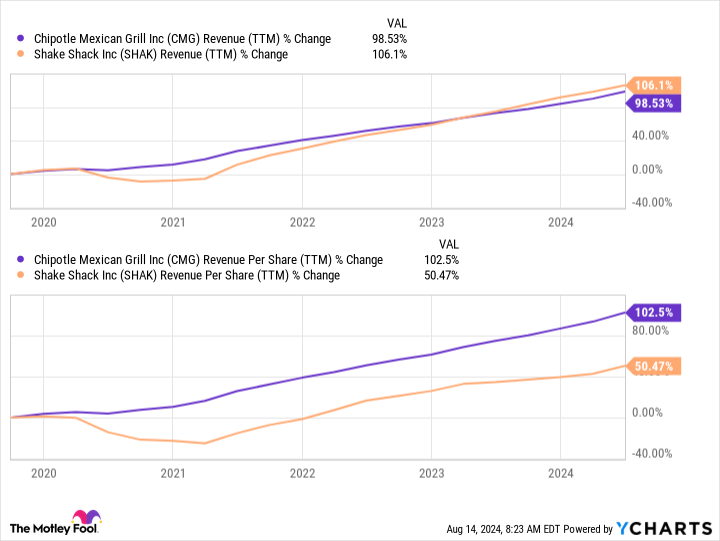

This is normal. The two chains have grown at a similar pace over the last five years with Shake Shack slightly outpacing Chipotle. But if you invested $1,000 in Chipotle stock five years ago, you’d have nearly $3,200 now. If you had done the same thing with Shake Shack stock, you’d have just $1,100 today.

Revenue growth is one of the most important things to look for when investing in stocks, but it’s far from the only thing. And one chart shows why Shake Shack’s growth hasn’t enriched its shareholders like it has for Chipotle investors.

The one chart you have to see to believe

When companies initially go public, they sell shares to investors to raise capital. But the share count changes thereafter. Companies can issue new shares to raise more money or pay employees, which increases the number of shares outstanding. And these companies can also use profits to repurchase shares from investors, which reduces the number of shares outstanding.

For its part, Chipotle has modestly reduced its share count over the last five years, while Shake Shack’s share count increased dramatically. Therefore, while the latter’s revenue has more than doubled, its revenue per share is only up about 50%.

Data by YCharts.

There’s no way to know for sure, but if Shake Shack’s share count had held steady or even decreased over the last five years, I would wager the stock would be beating the S&P 500 over this time. After all, its growth has been stellar. But the rising share count has diluted shareholder value, undoing much of the positive effect from its top line.

What about the next five years?

The good news here for Shake Shack shareholders is that things could be different over the next five years. The company offers stock-based compensation to managers to better align them with the company. But much of what’s happened in the past was related to an incentive plan adopted in 2015, and things are slowing down.

Last quarter, Shake Shack’s diluted-share count actually dropped on a year-over-year basis. Granted, management didn’t reduce the share count with share repurchases. Rather, some potential compensation has been forfeited.

Still, this does suggest Shake Shack is starting to turn the corner on this issue, meaning its revenue-per-share growth might soon more closely resemble its actual revenue growth. That could be a big deal.

As I mentioned, revenue growth is important for stocks. Shake Shack has growth in spades — it opened nearly 80 new locations over the past year, many of which are owned by the company. Revenue could continue to grow at a double-digit pace for years.

Moreover, Shake Shack is profitable, another important factor in how a stock performs. The company had operating income of nearly $11 million in its fiscal Q2. And with ongoing investment in technology to keep labor expenses in check, that number should climb higher.

To be clear, I’m not personally ready to give Shake Shack the benefit of the doubt. Investors can afford to be patient for now, waiting to see if recent trends continue. But I’m willing to watch the business more closely going forward because the company’s growth may finally be on the cusp of better rewarding shareholders in the coming years.

Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chipotle Mexican Grill. The Motley Fool recommends the following options: short September 2024 $52 puts on Chipotle Mexican Grill. The Motley Fool has a disclosure policy.

{kind=link}