Meta Platforms and MercadoLibre are off their all-time highs.

Finding some stocks that are a bit down to double up on can be a good investing strategy. However, investors must be sure that what they’re buying is a quality company that’s only down because the market has grown impatient or is expecting some short-term headwinds. If you can identify these companies, I think there is a lot of money to be made by purchasing shares today.

Two stocks that are a bit down that investors can double up on are Meta Platforms (META +0.50%) and MercadoLibre (MELI 0.93%). Both companions have bright futures ahead of them and can be purchased at a discount today.

Image source: Getty Images.

Meta Platforms

Meta Platforms is better known for the social media companies underneath its umbrella, like Facebook and Instagram. The primary revenue driver on these platforms is advertising, which is a high-margin business for Meta. Meta is also heavily investing in artificial intelligence (AI) to improve ad performance on its platforms, and it’s already seeing some of those benefits come about.

During Q3, revenue rose 26% year over year. With nearly all of its revenue coming from advertising-related sources, this showcases how strong this business is.

Today’s Change

(0.50%) $3.12

Current Price

$622.06

Key Data Points

Market Cap

$1567B

Day’s Range

$601.23 – $622.13

52wk Range

$479.80 – $796.25

Volume

1.6M

Avg Vol

14M

Gross Margin

82.00%

Dividend Yield

0.00%

However, the market is more concerned about what Meta is going to do with all of the cash it’s generating. During 2024, Meta spent about $39 billion on capital expenditures. For 2025, it estimates that it will spend $70 billion to $72 billion on capital expenditures, with nearly all of that money going toward AI data centers. Management stated that the dollar growth in capital expenditures will be “notably larger” in 2026, meaning that Meta is planning on spending at least $110 billion next year on capital expenditures.

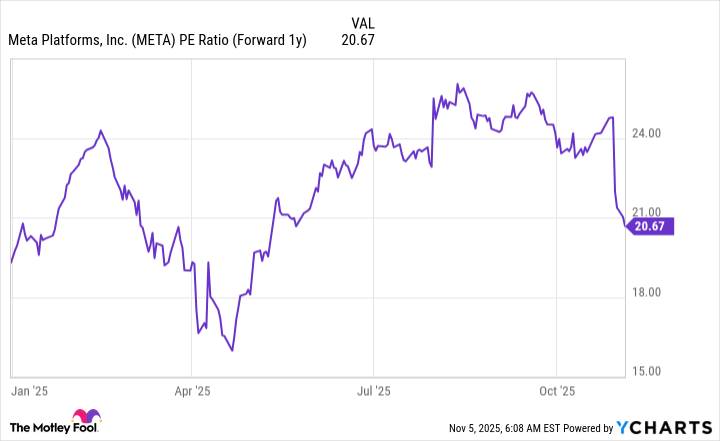

That’s a huge amount of money that Meta frankly doesn’t have, so it will need to take on debt, issue shares, dip into its cash balance, or find another way to finance this buildout. These plans spooked investors and caused the stock to tumble following earnings. Now, the stock trades for 21 times 2026 earnings.

META PE Ratio (Forward 1y) data by YCharts

Remember, this spending is only short-term in nature. If Meta decides that it’s done building out AI computing capacity, it will go back to being a cash-flow-generating machine, just like it was before the massive AI spending boom. I think this makes Meta a great stock to double up on while it’s down, as it may not stay low for long.

MercadoLibre

MercadoLibre has often been dubbed the Amazon of Latin America, but it also has a payment processing brand to go alongside it. The ecosystem that MercadoLibre has built in Latin America is impressive, and few have ever successfully challenged MercadoLibre in this region. Amazon tried multiple times, but ended up failing in the end. Still, investors are incredibly worried about Amazon’s renewed focus on Brazil, a key Latin American market. This has caused MercadoLibre’s stock to sell off a bit, and it’s down over 10% from its all-time high (at the time of this writing), although it has recovered from its recent lows.

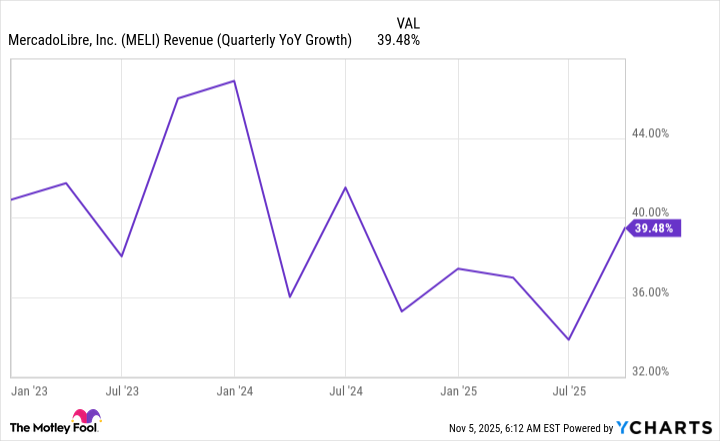

Still, I think there’s an excellent opportunity to invest in MercadoLibre, especially with the growth rates it’s putting up. MercadoLibre has historically been an incredibly fast-growing company, but its recent reacceleration is another reason to be excited about the company.

An investment in MercadoLibre is a bet that Latin America will continue to grow and expand its economic footprint. I think this is a very safe bet to make, and anytime you can pick up MercadoLibre on sale is a second chance of investing in a company like Amazon that has produced incredible returns for shareholders over the long term. Additionally, MercadoLibre isn’t a company that’s associated with the AI arms race, which is some diversification that may appeal to investors.

{kind=link}