If you’re looking for high-yield dividend stocks, I’ve got some good news. A couple of mortgage REITs offer eye-popping yields, and there’s a chance they’ll be able to maintain their payouts.

Shares of AGNC Investment (AGNC 2.37%) and Annaly Capital (NLY 2.53%) offer an average yield of 13.2% at recent prices. That means an investment of just $7,580 is enough to set you up with $1,000 in annual dividend income.

Before whipping out a brokerage application to buy these stocks, you should know that they are real estate investment trusts (REITs) that don’t own any real estate. Instead, they invest in mortgages and related financial instruments, which has all kinds of implications for investors seeking reliable dividend payments.

AGNC Investment

AGNC Investment is a mortgage REIT (mREIT). This means it makes a living by borrowing at relatively low short-term rates and investing in long-term mortgage-backed securities (MBS). The company makes monthly dividend payments, and at recent prices, the stock offers a huge 14.2% yield.

AGNC now offers a huge dividend yield because investors are worried about declining net interest spreads. The mREIT’s average cost of funds surged 373% higher to 2.89% during the two-year period that ended on Dec. 31, 2024. Investors are concerned that a new trade war could spark another round of inflation that would force the Federal Reserve to raise interest rates all over again.

One thing AGNC investors don’t have to worry about is mortgage defaults. As its name implies, the mortgages in its MBS portfolio are backed by government agencies that step in when borrowers can’t keep up with payments.

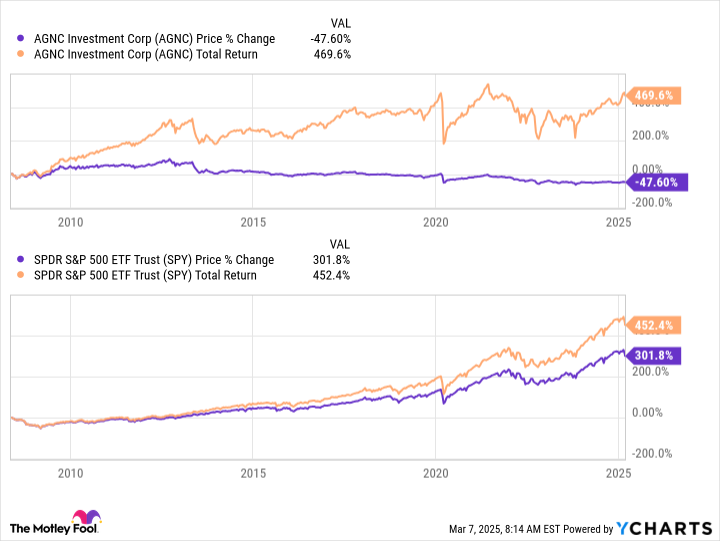

From its stock market debut in 2008 through March 6, 2025, AGNC’s stock price has declined by about 47.6%. By returning heaps of profits to shareholders as dividends, though, it has produced a total return of 470% since that debut. That’s a bit better than investors would have performed with an S&P 500 index fund over the same period.

Annaly Capital

Annaly Capital is another mREIT with a declining stock price and rising dividend yield. Like AGNC, Annaly stock is under pressure due to fears that the new trade war will start another round of inflation and force the Fed to hike interest rates. Lately, it’s been offering a 12.2% yield.

About 87% of Annaly’s $80.9 billion portfolio is invested in agency-backed securities. With the government ready to step in for most of its portfolio, fear of mortgage defaults isn’t an issue keeping Annaly’s shareholders up at night.

While AGNC focuses almost entirely on agency-backed MBS, Annaly has diversified its revenue stream. Its residential credit operation invests in non-agency mortgages and packages them into new securities. In 2024, it priced residential loan securitizations worth $11 billion.

In addition to a growing residential credit operation, Annaly has been investing in mortgage servicing rights. This is a great hedge against declining MBS expenses. In a nutshell, whoever owns servicing rights to a mortgage receives fees every time the borrowers make monthly payments.

In the fourth quarter of 2024, financing costs decreased. With the average cost of interest-bearing liabilities declining to 3.79%, net income on a generally accepted accounting principles (GAAP) basis reached $0.78 per share in the fourth quarter. That’s enough to support a dividend of $0.72 per quarter. If rates hold steady, maintaining its dividend payout at present levels probably won’t be an issue.

Know the risks

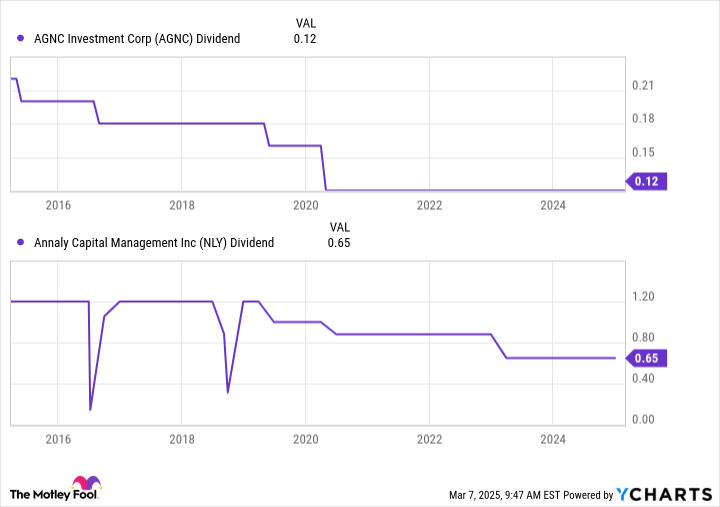

There’s a chance these two mREITs will maintain their dividends over the long run, but investors who need a reliable source of passive income will want to keep looking. A glance at their payouts over the past decade shows us why so few income-seekers find them acceptable.

AGNC Dividend data by YCharts.

Without any physical properties to borrow against, mREITs use their MBS portfolios to secure relatively low-interest loans. Unfortunately, the prices of long-term assets with fixed interest payments are sensitive to interest rate changes. When rapid rate changes lower the value of an mREIT’s collateral, they can be forced to sell assets at fire sale prices to boost liquidity and satisfy lenders. With a high sensitivity to interest rate changes they can’t control, most income-seeking investors are better off avoiding these stocks.

Cory Renauer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.