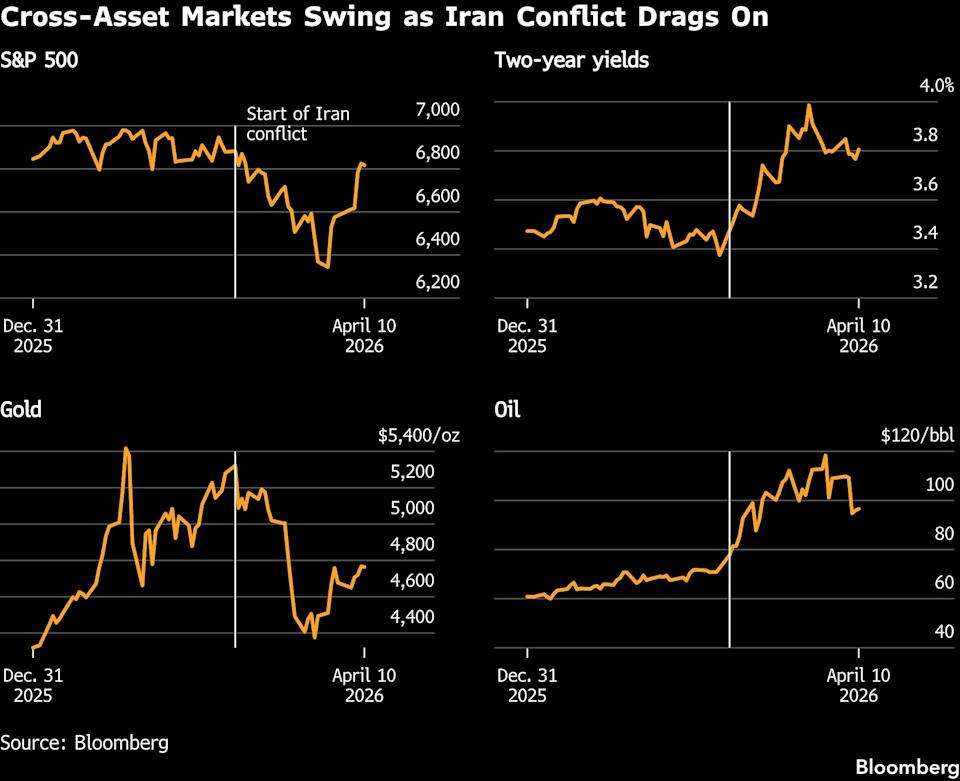

(Bloomberg) — The prospect that the Iran war will reintensify after the failure of peace talks threatens to spark fresh volatility across global markets, after a week that saw a fragile ceasefire drive stocks up and oil down by the most this year.

After the US and Iran were unable to reach a deal in negotiations over the weekend, President Donald Trump said the US will blockade the Strait of Hormuz. He posted on social media that “Any Iranian who fires at us, or at peaceful vessels, will be BLOWN TO HELL!” About a fifth of global oil and liquefied natural gas flowed through the waterway before the conflict.

The escalating rhetoric heightens the focus on the truce between the two sides, which triggered a sharp rally for risky assets last week, with the S&P 500 Index (^SPX) climbing more than 3.5%, an MSCI gauge of emerging-market equities rising 7.4%, and Bitcoin (BTC-USD) surging almost 10%. Futures on West Texas Intermediate oil tumbled 13.4% through Friday, while Brent ended at around $95 a barrel, down from roughly $112 in March.

Trading resumes in earnest for US stocks, Treasuries and oil at 6 p.m. New York time on Sunday. In early trading in Sydney to start the week, haven demand boosted the US dollar against major peers.

“The ‘peace dividend’ many traders priced in last Thursday and Friday is likely to evaporate” at the start of this week, said Francis Tan, Asia chief strategist at Indosuez Wealth in Singapore. “The failure of the talks shifts the mood back to defensive.”

Trump said the US will interdict any vessel that has paid a toll to Iran for safe passage through Hormuz and will clear mines in the strait. A blockade will add pressure to global oil markets by choking off the remaining trickle of shipments that have continued to move through the waterway.

Iran’s Islamic Revolutionary Guard Corps, meanwhile, responded by saying that any military vessels attempting to approach the strait “under any pretext” would be considered a violation of the ceasefire, according to Iranian state TV.

Handicapping how markets will react to ceasefire headlines has been a fraught process since the conflict erupted at the end of February. Big swings have been common as the US and Iran postured for negotiating advantage.

“Most investors that I know haven’t cut their positions — they are staying in the market but avoiding hard directional bets,” said Christophe Boucher, chief investment officer at ABN Amro Investment Solutions in Paris. “It’s a tricky situation as the downside potential is quite steep but one can’t afford to miss a rebound.”

{kind=link}