privetik

Dear Fellow Shareholders,

|

Annualized |

|||||||

|

Third Ave Real Estate Value Fund (Inst. Class) |

3Mo |

1Yr |

3Yr |

5Yr |

10Yr |

Inception |

Inception Date |

|

0.47% |

14.37% |

1.17% |

4.41% |

4.13% |

8.86% |

9/17/1998 |

|

|

Third Ave Real Estate Value Fund (Inv. Class) |

0.42% |

14.12% |

0.93% |

4.15% |

3.87% |

6.78% |

12/31/2009 |

|

Third Ave Real Estate Value Fund (Z Class) |

0.48% |

14.47% |

1.28% |

4.51% |

N/A |

3.38% |

3/1/2018 |

We are pleased to provide you with the Third Avenue Real Estate Value Fund’s (MUTF:TVRVX, the “Fund”) report for the quarter ended December 31, 2024. For the most recent calendar year, the Fund generated a return of +14.37% (after fees) versus +2.00% (before fees) for the Fund’s most-relevant benchmark, the FTSE EPRA NAREIT Developed Index¹.

The primary contributors to performance during the quarter included the Fund’s investments in (i) the preferred equity of Fannie Mae (OTCQB:FNMA) and Freddie Mac and (ii) the common stock of certain real estate operating companies (CBRE Group and Brookfield Corporation). However, these gains were partially offset by detractors during the period, including the Fund’s investments in businesses tied to residential construction (Lennar Corp., D.R. Horton, and Weyerhaeuser) and various U.K.based companies (Big Yellow, Segro plc, and Berkeley Group). Further insights into these positions, portfolio allocations, and the Fund’s additions to select international holdings (i.e., Berkeley Group, Big Yellow, and Accor SA) are included herein.

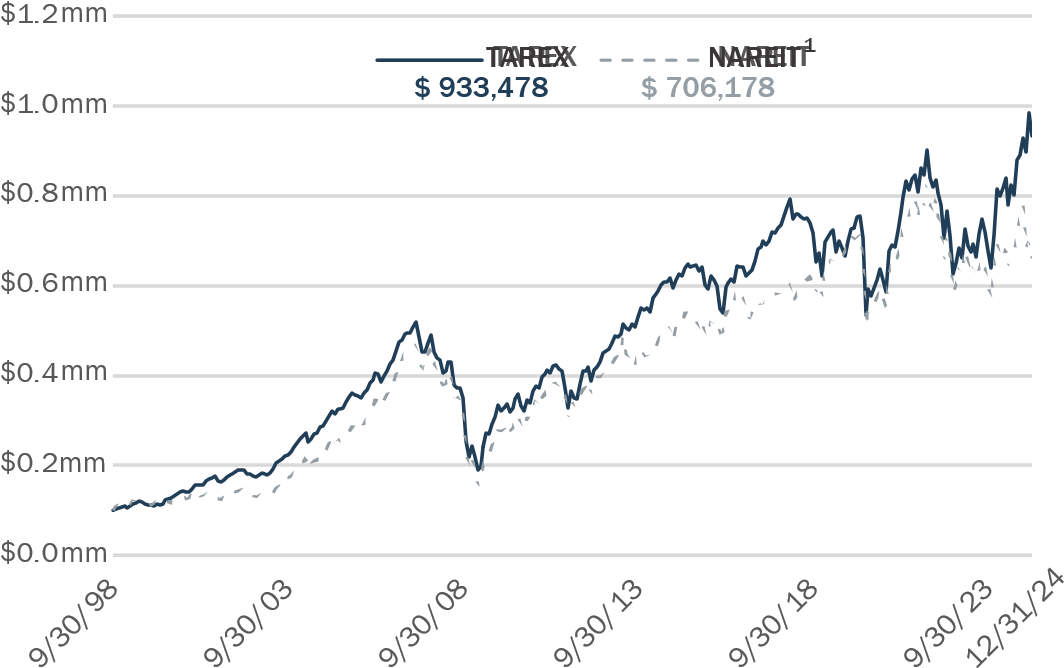

Notwithstanding recent performance, Fund Management considers the strategy’s long-term results as the most relevant scorecard. To that end, the Fund has generated an annualized return of +8.86% (after fees) since its inception more than twenty-six years ago. As a result, this performance indicates that an initial investment of $100,000 in the Fund would have a market value exceeding $930,000 (assuming distributions had been reinvested), or more than the same $100,000 would be worth had it been placed into a passive mutual fund tracking the Fund’s most-relevant benchmark over the same time-period.

VALUE OF $100,000 SINCE SEPTEMBER 1998: As of December 31, 2024

Hypothetical Investment since September 30, 1998 (Fund Inception Date September 17, 1998). Past performance does not guarantee future performance results.

Activity

In the Anatomy of the Bear: Lessons from Wall Street’s Four Great Bottoms, the ever-astute author Russell Napier studies four of the most significant “bear markets” in U.S. equities over the past century and sheds perspective on what led to these market disruptions. He also identifies “signals” that these stretches were near the end, thus paving the way for some of the “best returns” over the past 100 years.

As Napier illustrates, each period was generally idiosyncratic in nature. However, there were unifying factors with each occasion (i) preceded by overextended valuations when viewed through a fundamental lens and (ii) followed by a lengthy adjustment period as valuations declined for nearly a decade thereafter, on average. In addition, all four of the periods studied shared indicators that the “correction” was indeed ending, including: (i) incredibly “cheap equity prices”, which Napier measured by the “q-Ratio” (i.e., a measure of the stock market valuation relative to the replacement cost of its assets, similar to tangible book value) and (ii) low trading volumes, that subsequently increased alongside stock prices despite “continued declines in reported corporate earnings”.

While such findings are not directly related to real estate securities per se, Fund Management believes two primary concepts are relevant to the current market environment, as well as Third Avenue’s approach to investing in common stocks more generally, including:

- Diverging Valuations: It is widely reported that most “broad based” equity indices are trading at above-average price-to-earnings (“P/E”) multiples within a historical context, particularly with the expanding concentration of the “Magnificent 7” in such composites. What seems less reported though, in our view, is that certain sub-sets of these indices have diverged significantly in recent years. For instance, the MSCI USA Index (which tracks the midand-large cap segments of the U.S. equity markets) currently trades at a price-to-book multiple of 5.2 times— more than 50% above the long-term average and a level that has only been exceeded in one other instance in the past 30 years (i.e., Q1 2000). On the other hand, distinct sub-sets of global equities remain much more modestly valued and below long-term averages, such as Listed Real Estate (as measured by the MSCI ACWI Core Real Estate Index) and International Equities (as measured by the MSCI EAFE Index), which currently trade at price-to-book multiples of 1.3 times and 1.8 times, respectively.

- Fundamentals over Technicals: Despite Napier identifying certain “signals” that tend to precede a recovery in equity prices after market bouts, Fund Management does not believe it is possible to “pick market bottoms” with precision (e.g., March 2009). In lieu of such an endeavor, the Real Estate Value Fund concentrates its common stock investments in enterprises that are not only trading at discounts to Net-Asset Value (“NAV”), but ones that are also remarkably well-capitalized and run by aligned control groups. While such a tradeoff may leave the Fund establishing positions in securities that “drift lower” in the near-term, it has been our experience that well-established real estate platforms are likely to prove more durable in value over the long-term.

Along these lines, the Fund increased its allocation to a region within Listed Real Estate that has diverged sharply from a fundamental valuation standpoint more recently: the U.K. & Europe. Fund Management recognizes the various currents on the political, social, and economic front in these markets. However, the price-to-value gap for several issuers seems to compensate for such items, in our opinion, and led to the Fund increasing certain holdings in the quarter, including: Berkeley Group (OTCPK:BKGFY), Big Yellow (OTCPK:BYLOF), and Accor SA (OTCPK:ACRFF).

The Berkeley Group Holdings PLC (“Berkeley”) is a U.K.-based real estate operating company focused on residential-led regeneration projects in London and Southeast England. It is also one of the premier real estate platforms globally, in our view, as Berkeley is (i) extremely well-capitalized with a netcash position and an unrivaled land bank with planning for more than 50,000 homes in exceptionally supply-constrained markets, (ii) very well-managed by a team that not only owns significant stock but has an excellent capital allocation track record, and (iii) compounding its corporate net-worth by more than 10% per year, on average, through efficient operations where it accounts for nearly 1 out of every 10 new homes built in London.

In addition, Berkeley’s common stock traded at less than 10 times earnings by Fund Management’s estimates and a priceto-book multiple of 1.1 times—essentially the lowest implied ratio in the past 15 years. Notwithstanding, Fund Management expects that Berkeley common will trade back in-line with its “run-off value” at the very least as interest rate (and mortgage rate) volatility in the U.K. subsides. In the meantime, the company is unlocking additional value by forming a privaterental or “PRS” platform as well as returning capital to shareholders through accretive share repurchases and special dividends.

Big Yellow (“Big Yellow”) is a U.K.-based Real Estate Investment Trust (“REIT”) that owns and operates a portfolio of 109 self-storage facilities that span 6.4 million square feet of total space and are concentrated in London. The company also represents one of the most compelling opportunities in commercial real estate, in our view, as Big Yellow is (i) very well-capitalized with a hard-to-replicate platform of Londoncentric self-storage facilities that are modestly encumbered with a loan-to-value ratio of less than 15%, (ii) run by the founding members who have adhered to a “balanced approach” over the past two decades, and (iii) capable of increasing its cash flows (and value) by more than 10% per year as it renews in-place leases, fills existing vacancy, delivers new developments, and benefits from the operational leverage and scale efficiencies associated with self-storage.

At the same time though, Big Yellow’s common stock traded at prices that implied a 7.5% “capitalization rate” at quarter-end (or the unlevered yield on the real estate assets) without factoring in any value for the further lease-up of the in-place portfolio despite a vacancy rate of nearly 20%. The shares also trade at a price-tobook multiple of approximately 0.7 times—the lowest level in more than a decade. With this being the case, Fund Management expects the price-to-value gap to narrow as Big Yellow continues to execute on its measured expansion and fundamentals stabilize. If not, Big Yellow could very well get wrapped up into industry consolidation where private market transactions have implied significantly lower cap rates (and thus significantly higher asset values) more recently.

Accor SA (“Accor”) is a France-based hotel management and franchise company with a global hospitality platform that comprises nearly 5,000 hotels and 850,000 rooms— approximately 95% of which are in Europe, the Middle East, Asia Pacific, and South America. In Fund Management’s opinion, the company is also one of the few “safe and cheap” opportunities in the lodging space as Accor is (i) wellcapitalized with the largest y platform outside of North America, which is also cash generative and modestly encumbered, (ii) run by an aligned control group including a knowledgeable and engaged shareholder base, and (iii) actively creating value by monetizing owned real estate and redirecting capital to further expanding its “management and franchise” business, particularly outside of North America where the shift to such platforms is accelerating.

Notwithstanding this progress, Accor’s common stock seems to remain at a meaningful discount to its NAV and global peers. Put otherwise, when one accounts for the value of the company’s investments in certain partially owned assets (i.e., AccorInvest), the implied value for the remaining management and franchise platform is approximately 13 times cash flow by our estimates, more than a 40% discount to its global peers. Therefore, Fund Management believes Accor’s cost of capital will improve as it completes the transition to an “asset light” global hospitality platform. If not, it would not be inconceivable to see the company engage in resource conversion by combining its business (or one of its segments) with other industry participants to surface value.

Outside of these additions, the Fund also trimmed back various positions for portfolio management purposes, including: CBRE Group (CBRE), Brookfield Corp. (BAM), Fannie Mae, and Freddie Mac. Fund Management remains constructive on each holding however, and would note recent developments at Fannie Mae and Freddie Mac (collectively the “GSEs”) as particularly supportive of the team’s long-held investment thesis. That is to say, the GSEs seem to be moving closer to exiting “conservatorship” having accumulated nearly $150 billion of “net-worth”, with the potential for that timeline to be accelerated as contemplated by the Congressional Budget Office in this December 2024 Report: An Update to CBO’s Analysis of the Effects of Recapitalizing Fannie Mae and Freddie Mac Through Administrative Actions.

In addition, the Fund (i) received a special dividend from Timber REIT Rayonier Inc. (RYN) and (ii) extended out hedges relating to certain foreign currency exposures (i.e., British Pound) during the period. Also of note: the Fund’s long-time holding Lennar Corp. (LEN, a U.S. homebuilder) finalized plans to “split off” its land development business (“Millrose Properties”), with the transaction to be effectuated in mid-January. Fund Management believes the separation will surface incremental value for Lennar Corp. as a “net cash” and “land light” builder following the deal and plans to share further details in the next Shareholder Letter.

POSITIONING

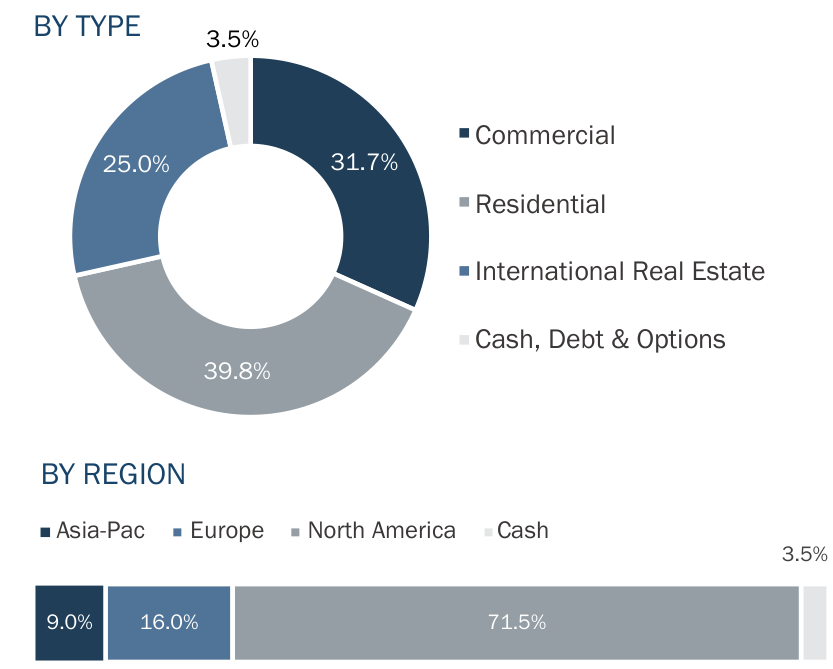

After incorporating this activity, the Fund had approximately 39.8% of its capital invested in U.S.-based companies focused on Residential Real Estate, including those involved with: Entry-Level Homebuilding (Lennar Corp. and D.R. Horton); Workforce Housing (AMH and Sun Communities); Land and Timber (Rayonier, Weyerhaeuser, and Five Point); and Mortgage and Title Insurance (Fannie Mae, Freddie Mac, and Fidelity National Financial). In Fund Management’s view, each one of these enterprises has a well-established position in its respective segment of the residential value chain. In addition, these holdings seem poised to benefit from favorable fundamental drivers within the U.S. residential markets over time, including: (i) near record low levels of for-sale inventories, (ii) near record high demand for affordable for-sale and rental options, and (iii) cost pressures leaving more-efficient industry participants taking further market share.

The Fund also had 31.7% of its capital invested in North American-based companies involved with select pockets of Commercial Real Estate, including: Real Estate Services (CBRE Group and JLL); Asset Management (Brookfield Corp. and Brookfield Asset Mgmt.); Industrial and Logistics (Prologis, First Industrial, and Wesco); and Self-Storage (U-Haul Holdings). In Fund Management’s opinion, these holdings represent platforms that would be very difficult to reassemble. They also comprise areas of commercial real estate that seem to favor long-term investors. Put otherwise, these enterprises concentrate on either (i) property types with structural demand drivers and limited “maintenance capex” or (ii) real estate services that are generally less “capital intensive” with a focus on brokerage, property management, and other advisory activities that can offer “higher returns on invested capital” over time.

An additional 25.0% of the Fund’s capital is invested in International Real Estate companies. These businesses are largely focused on the same types of residential and commercial activities as outlined above, simply with leading platforms in their respective regions. At the end of the quarter these investments included issuers involved with: Commercial Real Estate (CK Asset, Big Yellow, National Storage, Wharf and Segro); Residential Real Estate (Berkeley, Grainger, and Ingenia); and Real Estate Services (Savills and Accor). The holdings are also listed in developed markets where Fund Management believes there are (i) adequate disclosures and securities laws as well as (ii) ample opportunities for resource conversion and change of control transactions (e.g., the U.K., Australia, France, and Hong Kong).

The remaining 3.5% of the Fund’s capital is in Cash, Debt & Options. These holdings include U.S.-Dollar based cash and equivalents, short-term U.S. Treasuries, and hedges relating to certain foreign currency exposures (i.e., Hong Kong Dollar and British Pound).

The Fund’s allocations across these various segments are outlined in the chart below, along with the exposure by geography (North America, Europe, and Asia-Pacific). In addition, the holdings continue to represent “durable value” in Fund Management’s opinion. That is to say, the equity holdings are very well capitalized (in our view) with an average loan-to-value ratio of 14% at the end of the period. Further, the discount to NAV for the Fund’s holdings expanded to 20.9% at quarter-end when viewed in the aggregate.

ASSET ALLOCATION As of December 31, 2024 | Source: Company Reports, Bloomberg

FUND COMMENTARY

During the quarter, the Federal Reserve Bank of Cleveland published an economic commentary titled New-Tenant Rent Passthrough and the Future of Rent Inflation. While certainly not an “attention getting” headline in most circles, the analysis had important implications in Fund Management’s view. Most importantly, the co-authors observed that in the U.S. the “year-over-year consumer price index (CPI) inflation rate—excluding shelter—is below 2.0%” whereas the “year-over-year CPI shelter inflation rate is 4.8% and the largest component of CPI inflation with a weight of about 32%”.

The co-authors also noted the “year-over-year figures” for shelter have not correlated to other widely followed benchmarks tracking rental rates nationwide. Instead, the coauthors concluded this disconnect was due to the “CPI figure placing a larger weight on existing tenants” as opposed to “new move-in rates”. Notably, they also estimated that a nearly 5.5% gap between in-place rents and market rents remained for existing tenants. As a result, the analysis concluded that “CPI rent inflation will remain above its prepandemic norm of about 3.5% until mid-2026”.

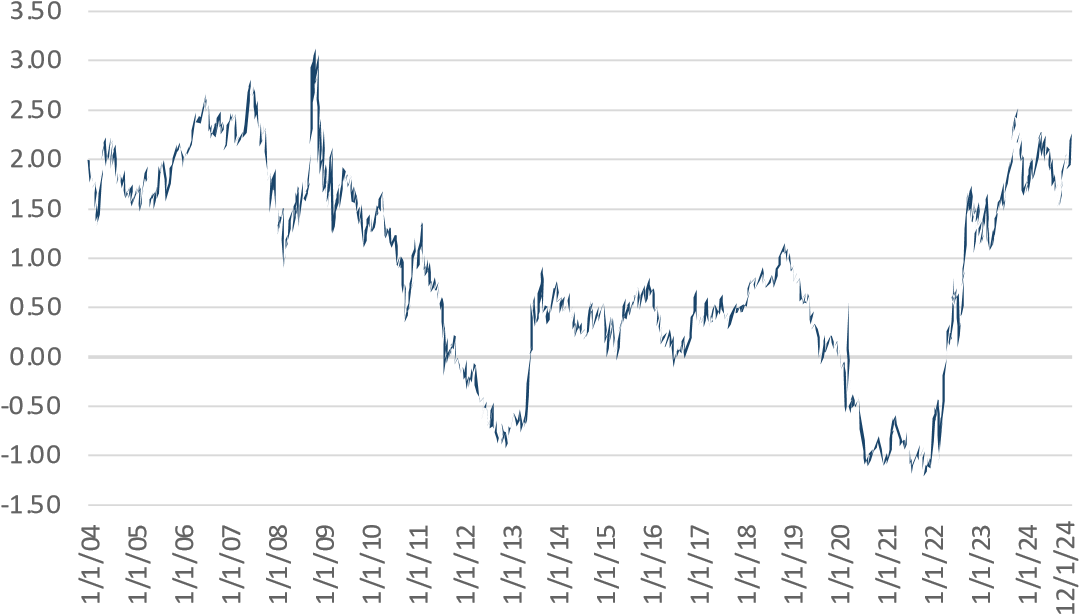

At the same time, investors in long-dated U.S. Treasury Notes (e.g., 10-Year and 30-Year Notes) experienced another year of “mark-to-market” losses in 2024. In fact, this represents the fourth time in the past five years that such an outcome has transpired. Consequently, it appears as if fixed-income investors have begun to demand structurally higher “real rates of return”, or a greater return premium over the prevailing inflation rate. For perspective, the chart below illustrates that the “real rate of return” for 10-Year U.S. Treasury Notes (US10Y) exceeded 2.0% at the end of 2024—a level that is well above those offered in the decade following the “global financial crisis”.

10-Year U.S. Treasuries: Real Rates of Return As of December 31, 2024 | Source: Federal Reserve

When the potential for higher rates of CPI as noted by the Cleveland Fed is viewed in combination with the seeming reset in “real rates”, it is not inconceivable to expect that nominal yields for U.S. Treasuries (i.e., the sum of the real rate and the inflation rate) will remain more elevated in the period ahead. Therefore, Fund Management believes that three factors will remain paramount for generating differentiated results in Listed Real Estate, including a focus on holdings that exhibit:

- Financial Strength: In our experience, well-financed businesses can not only navigate through more challenging markets, thus preserving value, but are also positioned to make value-enhancing investments when capital is scarce. In other words, the Fund targets real estate businesses with super strong financial positions. In fact, at the end of the year the Debt to Asset Ratio for the Fund’s holdings was 40% less than those of the constituents comprising the largest Real Estate Mutual Fund: the Vanguard Real Estate Index Fund (VGSNX). In addition, the Fund’s holdings seem less dependent upon capital markets to finance capital allocation priorities. This is largely due to the Third Avenue Real Estate Value Fund being focused on enterprises that can retain cash flow to reinvest in the business with more than 70% of the portfolio structured as Real Estate Operating Companies (“REOCs”) versus REITs (which are required to distribute most of the cash flow as dividends).

- Durable Value: Real Estate remains a contrarian allocation with generalist investors still “underweight” the sector per BofA Research. Not a coincidence, Listed Real Estate seems to trade at more favorable valuations with the Price to Funds from Operations (“FFO” or a Real Estate measure of cash flow) for U.S. REITs at 19 times per Citigroup research—more than a 30% discount to the P/E ratio for broader U.S. equites as measured by the MSCI US Index. Such a disconnect is rare. However, balanced observers would point out that REITs face various headwinds, including the need to refinance debt at higher rates, which is likely to offset “top line” growth in many instances. As an alternative, the Real Estate Value Fund’s holdings not only trade at a discount on cash flow metrics, but also conservative estimates of NAV. The Fund’s holdings also traded a price-to-book ratio of 1.3 times at quarter-end, compared to the VGSNX at 2.4 times at the same date.

- Prospects to Increase NAV: Third Avenue’s Founder Marty Whitman once said, “If the NAV isn’t growing, the NAV is wrong”—which we believe he would agree is even more so the case in a higher “real rate” environment. Within that framework, the other unifying theme behind the Fund’s investments across the Residential, Commercial, and International Real Estate segments is that the holdings operate in real estate sectors that seem to be structurally supported with (i) favorable supply-and-demand dynamics or (ii) industry forces that favor further consolidation. As a result, the select-set of issuers held in the Real Estate Value Fund seem to exhibit “pricing power” or distinct “operating leverage”, leaving them less dependent upon nominal inflation (or negative real rates) to increase revenues (and profits) in our assessment.

Fund Management recognizes an emphasis on these factors will not likely prove to be the optimal strategy should a period of “negative real rates” resurface (i.e., when significant leverage tends to be rewarded). However, a focus on (i) wellcapitalized businesses, (ii) with discounted security prices, and (iii) prospects for further wealth creation is a combination that has always made sense at Third Avenue. It is also a strategy that seems particularly well-suited for those seeking out “Real Returns” in Listed Real Estate in the period ahead.

We thank you for your continued support and look forward to writing to you again next quarter. In the meantime, please don’t hesitate to contact us with any questions or comments at [email protected].

Sincerely,

The Third Avenue Real Estate Value Team

|

This publication does not constitute an offer or solicitation of any transaction in any securities. Any recommendation contained herein may not be suitable for all investors. Information contained in this publication has been obtained from sources we believe to be reliable, but cannot be guaranteed. The information in this portfolio manager letter represents the opinions of the portfolio manager(s) and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed are those of the portfolio manager(s) and may differ from those of other portfolio managers or of the firm as a whole. Also, please note that any discussion of the Fund’s holdings, the Fund’s performance, and the portfolio manager(s) views are as of December 31, 2024 (except as otherwise stated), and are subject to change without notice. Certain information contained in this letter constitutes “forwardlooking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof (such as “may not,” “should not,” “are not expected to,” etc.) or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of any fund may differ materially from those reflected or contemplated in any such forward-looking statement. Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders. Date of first use of portfolio manager commentary: January 15, 2025 1 The FTSE EPRA/NAREIT Developed Real Estate Index was developed by the European Public Real Estate Association (EPRA), a common interest group aiming to promote, develop and represent the European public real estate sector, and the North American Association of Real Estate Investment Trusts (NAREIT), the representative voice of the US REIT industry. The index series is designed to reflect the stock performance of companies engaged in specific aspects of the North American, European and Asian Real Estate markets. The Index is capitalization-weighted. The index is not a security that can be purchased or sold. For the Third Avenue Glossary please visit here. Allocations are subject to change without notice Past performance is no guarantee of future results; returns include reinvestment of all distributions. The above represents past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance, please visit the Fund’s website at Third Avenue Management | Pioneers in Value Investing Since 1986. The gross expense ratio for the Fund’s Institutional, Investor and Z share classes is 1.19%, 1.45% and 1.11%, respectively, as of March 1, 2024. Distributions and yields are subject to change and are not guaranteed. Risks that could negatively impact returns include: overbuilding and increased competition, increases in property taxes and operating expenses, lack of financing, vacancies, environmental contamination and its related clean-up, changes in interest rates, casualty or condemnation losses, and variations in rental income. The fund’s investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling 800-443-1021 or visiting Third Avenue Management | Pioneers in Value Investing Since 1986. Read it carefully before investing. Distributor of Third Avenue Funds: Foreside Fund Services, LLC. Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders. Third Avenue offers multiple investment solutions with unique exposures and return profiles. Our core strategies are currently available through ’40Act mutual funds and customized accounts. If you would like further information, please contact a Relationship Manager. Performance is shown for the Third Avenue Real Estate Value Fund (Institutional Class). Past performance is no guarantee of future results; returns include reinvestment of all distributions. Past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance, please visit the Fund’s website at Third Avenue Management | Pioneers in Value Investing Since 1986. The U.S. Lipper Fund Award for Best Equity Small Fund Family is based on a review of 185 qualified fund management companies that were eligible for the three-year period ending on 11/30/23. To qualify for Lipper’s Overall Small Fund Family Group Award, Small fund family groups must have at least three equity portfolios. The group award will be given to the group with the lowest average decile ranking of its respective asset class results based on the three-year Consistent Return measure of the eligible funds. From LSEG Lipper Fund Award© 2024 LSEG. All rights reserved. Used under license. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}