I don’t shy away from chasing world-class returns—and right now, artificial intelligence (AI) is the booming market of our generation rather than a passing trend. AMD represents one of the best routes to capitalizing on the information revolution powered by AI. Veteran stock investor Charlie Munger has often said how a patient “surfing” strategy can help investors find truly stellar-returning stocks. The key is to choose wisely and resist the temptation to jump off.

Don’t Miss Our End of Quarter Offers:

That’s why I’m maintaining my bullish stance on Advanced Micro Devices (AMD) stock, among other flagship AI names. Given the ongoing market correction, including AMD’s 15% slide since January, marked so ominously by today’s “Liberation Day,” AMD entry prices have dropped back to affordable levels.

The way this stock can move—snapping upward in a matter of months—is remarkable. From where things stand, I believe the stock can double over the next twelve months. In my view, the broader market will catch on soon enough—but for now, picking up superb tech stocks on the cheap and ahead of the curve could lock in prices most investors will be jealous of six months from now.

Betting Big and Strategically on the AI Boom

We’re in the middle of an unprecedented AI boom that simultaneously offers innovation and disruption. According to market research from McKinsey, global demand for data center capacity could triple by 2030—in a bearish case—and nearly 70% of that growth could be driven purely by AI workloads. Some skeptics are already calling it a bubble.

Even AMD—sitting front and center in this shift—keeps revising its projections higher. In mid-2023, it estimated the data center AI accelerator market would hit $400 billion by 2027. Just months later, after demand for generative AI skyrocketed, that estimate was bumped to $500 billion by 2028. That’s sustained annual growth of 60-70%. In other words, the AI rocket ship still has plenty of fuel.

Charlie Munger has often said the secret to getting rich is surfing–catching a big wave and riding it all the way: “When new businesses come in, there are huge advantages for the early birds. And when you’re an early bird, there’s a model that I call ‘surfing.’ When a surfer gets up and catches the wave and stays there, he can go a long, long time. But if he gets off the wave, he becomes mired in shallows. People get long runs when they’re right on the edge of the wave— whether it’s Microsoft or Intel or all kinds of people, including National Cash Register in the early days.”

AI isn’t just a wave—it’s a tidal surge of capital and innovation. A once-in-a-generation opportunity to build real wealth. Still, even the biggest waves can crash. With rising geopolitical tensions—especially between China and Taiwan—there’s a real risk of supply chain disruption. Taiwan is home to TSMC (TSM), the linchpin of global chipmaking. If a blockade or invasion were to occur, some models suggest global markets could fall by 50-90%, with the tech sector hardest hit.

To mitigate the risks, I’m holding 30% of my portfolio in cash equivalents. I remain bullish on AMD and AI as a sector, but I’m also cognizant of keeping a life raft in case the tide turns. My cash buffer allows me to buy the dips if things stay steady. If a crash hits, I’ve got the liquidity to remain calm—and strike when others are forced to retreat.

AMD’s Near-Term Upside

Stock prices do not move based on logic alone—they trade on sentiment. Right now, market sentiment is gripped by uncertainty and fear. Equity investors are clearly rattled between talk of tariffs and potentially worsening macro data due to an impending trade war. But I don’t think the fearfulness will last. I’m forecasting a 3.5% Fed rate by the first half of 2026, which should help risk-on sentiment return.

Zooming out just a little, Big Tech is on track to pour $350 billion into AI capex next year. That’s not incremental—it’s a full-on infrastructure buildout. When you combine that level of investment with strong fundamentals, AMD stock may have an inherent price floor driven by organic future demand.

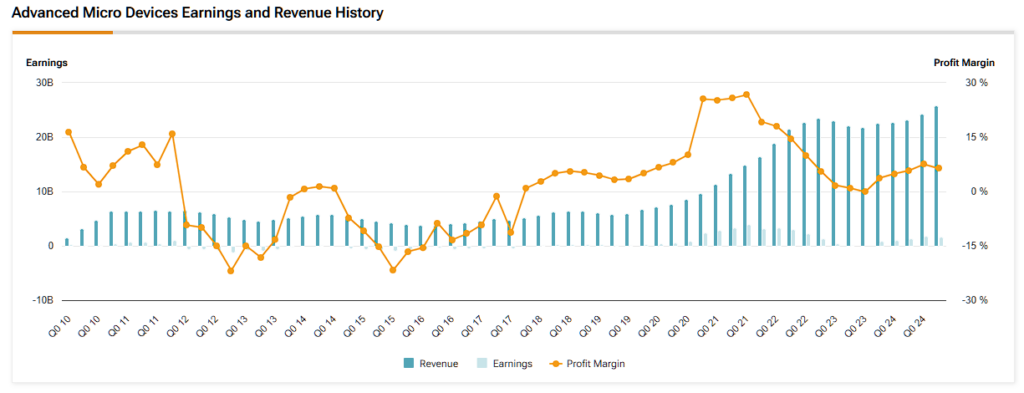

Even if AMD doesn’t fundamentally deserve to hit $215 per share until FY2027, the market is a forward-pricing machine. It typically prices in growth several months in advance. So, that valuation could appear by 2026. For AMD to hit $215 per share, it would need to reach $45 billion in revenue by FY2027, posting a 30% net margin and increase to 1.9 billion shares outstanding. This would result in $13.5 billion in net income—or roughly $7.11 in earnings per share. Apply a price-to-earnings ratio of 30 (still below Nvidia’s multiple of 35), and you get a $215 price target.

The market may be irrational—but that’s where opportunity lives. While speculators flinch at the headlines, investors focus on the fundamentals. And in AMD’s case, those fundamentals are only getting stronger.

Is Advanced Micro Devices a Buy or Sell?

Wall Street’s already warming up to AMD. AMD stock carries a Moderate Buy consensus rating based on 24 Buy, 12 Hold, and one Sell ratings over the past three months. AMD’s average price target of $146.87 per share implies approximately 43% upside potential over the next twelve months.

Current AMD Consolidation Phase Set for Eventual Expansion

Sitting out the current AI boom could be a costly mistake. However, FOMO is not a trading strategy. Yes, this space is volatile—there’s no denying that. But volatility is the cost of entry when you’re chasing generational upside. For investors with patience and a strong stomach, riding through the bumps often leads to abnormal returns in the long run.

Of course, risk management matters. Protecting yourself from sudden shocks is key, so I always keep a healthy cash buffer and some gold on hand. But zooming out, AI remains an embryonic sector with market maturity at least a decade away. With AMD stock trading at just 5x forward sales and right in the middle of the AI computing revolution, going bullish is a no-brainer.

Source link