How inequality and international tension interact is an urgent question for the early 21st century – hence the current preoccupation with global imbalances. For many interpreters of our conjuncture, it seems that we are regressing both in terms of inequality and international tension to a configuration alarmingly reminiscent of the pre-1914 era. The inequality numbers in the US resemble those of the gilded age. And then there is the Thucydides trap argument about how jealous incumbents foment tension so as to stop the rise of potential challengers. In 1914 the British Empire was supposedly positioned in that role, warding off Imperial Germany. Today it is the USA facing the rise of China.

In Class Wars are Trade Wars, Pettis and Klein draw explicitly on J.A. Hobson, whose book Imperialism (1902) provided an inspiration for Lenin’s later writing on imperialism. Hobson, a radical liberal, argued that the distribution of domestic income, wealth and power favoring elites in rich countries, notably Imperial Britain, created an macroeconomic impasse – underconsumption – which forced them aggressively to export capital to generate demand for underused industrial capacity. That capital export led to imperialist conflict. Hobson’s immediate inspiration was the Boer War (1899-1902), in which British state power was mobilized in support of giant investor interests in South Africa against the earlier generation of Boer colonists and their international backers.

For Hobson this imperialism was a new phenomenon, sharply to be distinguished both from settler-colonial projects that had begun in the early modern period and from the relatively benign and even-handed age of Imperial dominance that he projected into the mid 19th century. Imperialism came after Empire. The new, dog-eat-dog, zero-sum world, in which the very existence of major powers could be put in question (Paul Schroeder’s key insight regarding 1914), was one that had come into view in the late 19th century with the closing of the global frontier, the rise of a hungry new generation of nation states and the extreme domestic inequality of the gilded age.

Pettis and Klein see similar dynamics at work in the early 21st century. Their key point is that distributional struggle in China – huge inequality imposed by the CPC regime and its cronies in big business – and other export surplus countries (Germany in its new era of neoliberalism from the early 2000s) spills over into trade surpluses and capital exports. These constrain options for other players in the system that do not engage in wage repression, currency manipulation or capital account controls. In this manipulated globalization regime, it is the US with its endless consumer demand and huge financial markets that ends up absorbing the surpluses of other countries.

The result, after 2000s, is mounting trade tension as socio-economic forces in the United States push back against the exorbinant burden of being the world’s export market. Thankfully, Pettis and Klein do not go so far as to declare inter-imperialist war inevitable. As they rightly insist, the implications of Hobson’s theory were optimistic. The source of the problem was the distortion of the power balance in the surplus countries. If the right internationalist coalition can be organized against elites and rentiers on all sides, then the maldistribution of income and with it chronic maldistribution of demand can be corrected.

What goes underemphasized in this creative reworking of Hobson for the 21st century – especially when Pettis and Klein are twinned with the Thucydides trap argument – are the head-turning differences between the world that Hobson and his contemporaries were criticizing and the world which we inhabit today.

The object of Hobson’s critique was after all the British empire, the dominant player in the international system. It was Britain that was generating the surpluses and pouring capital into the rest of the world. The main object of Pettis and Klein’s critique, by contrast is not the US, but subordinate players like Germany and up and coming emerging markets like China. In Pettis and Klein, it is China’s capital export and America’s capital import that are the cause of tension. China is undeniably mighty, but it is not the incumbent. It is the challenger.

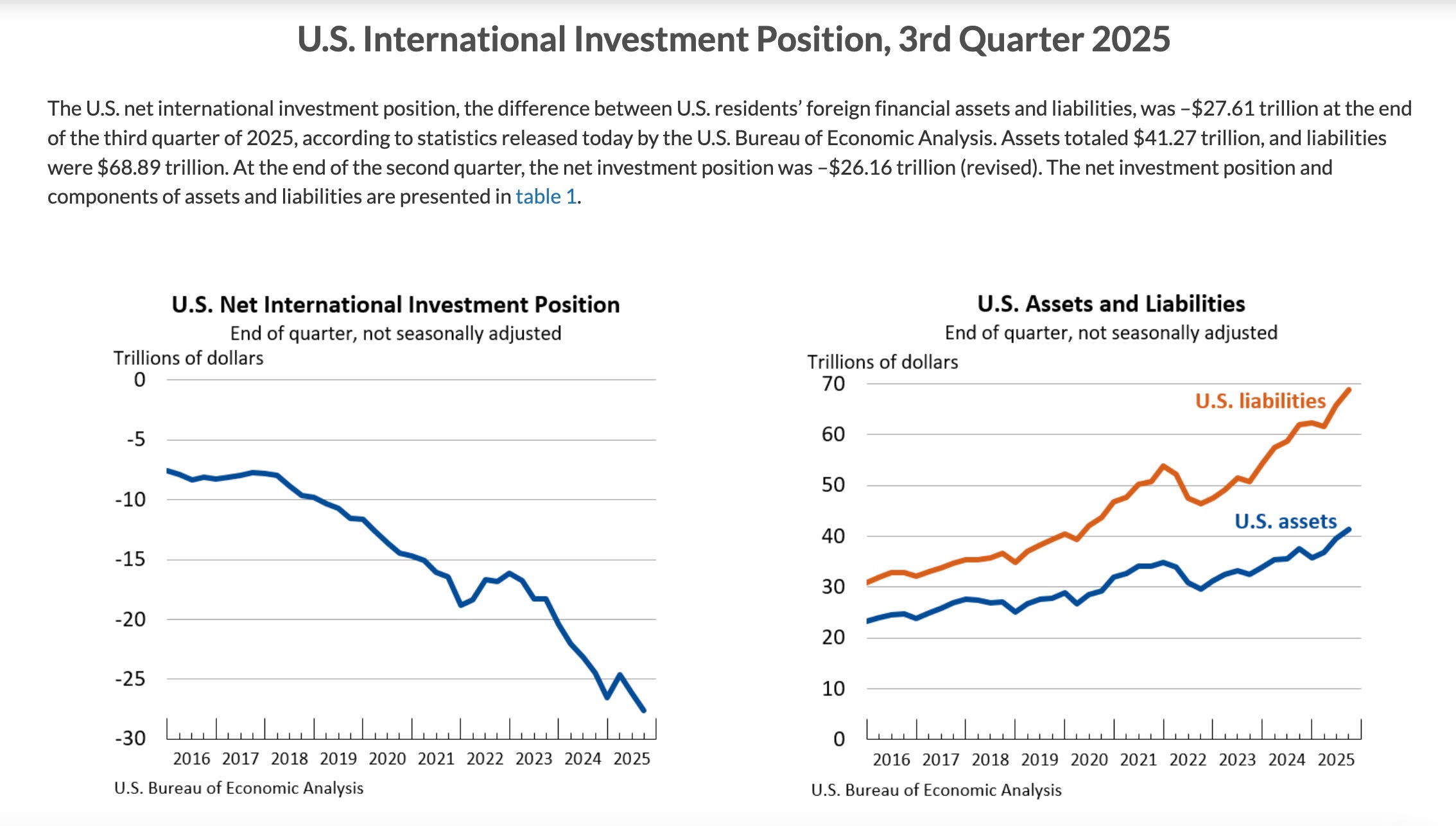

Pause for a moment to consider what is going on here. In the 21st century, the “richest country” is a net borrower not a lender – the opposite of Edwardian Britain’s position. In the 21st century, net investment is flowing uphill: from middle income (in the case of China) or lower high-income (in the case of AE lenders) towards the apex, which is Wall Street and the high-income USA.

Source: BEA

In Hobson’s world, the flows were the other way around. Whatever else was wrong about the world before 1914 this at least “made sense”. Investment was flowing “downhill” from the metropole to the developing periphery. In per capita terms capital-recipient countries like Argentina in the early 1900s were far from poor. But they were developing (Suggesting a question about the USA today which I will return to in a later post). In the Hobson-Lenin thesis, It was the rivalrous bidding by competing rich countries to drive imperial development that was the source of international tension. This struggle to lead development is precisely the kind of struggle that some imagine might be taking place today – when they call, for instance, for a new green Marshall Plan. But, de facto, China is the only game in town.

Pettis and Klein are, I am sure, fully aware of these differences. Theirs is not a carbon copy of Hobson’s critique so much as a mirror image of it, for our “hall of mirrors” world. But especially when their thesis is combined with the Thucydides Trap, heads are easily turned. So it is worth underlining in bold just how dramatic the differences between the 1910s and the 2020s are.

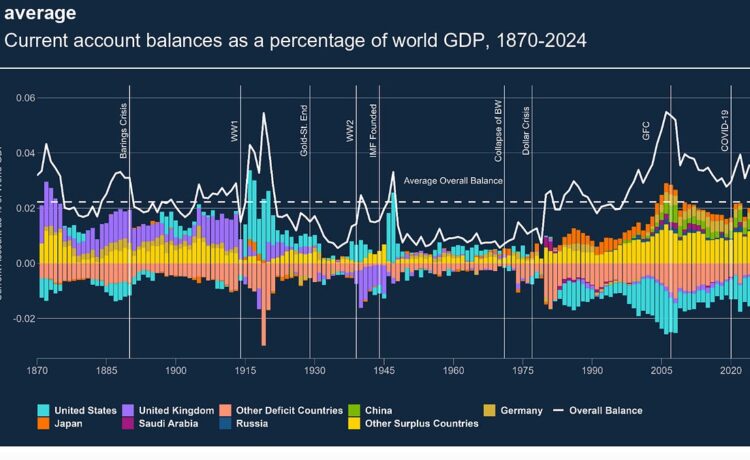

The gold peg before 1914 was general, so, no fiat currencies and only moderate scope for macroeconomic policy. The free flow of capital was unimpeded, as was the free flow of labour for Europeans. Nevertheless, the scale of British capital export – Hobson’s key point of critique – was gigantic. Long-run data series produced by the Bank of England as part of its contribution to the current debate about global imbalances, paint the picture in stark terms. Over the forty-plus years between 1870 and 1914, the UK – the incumbent hegemon, not the up and coming challenger – was a larger capital exporter in relative terms, than Japan and China have been since the 2000s. As the purple segment in this graph shows, over the 150 year history of the modern world economy there has never been another capital exporter that matched the outflows of Victorian or Edwardian Britain.

Source: Bank of England

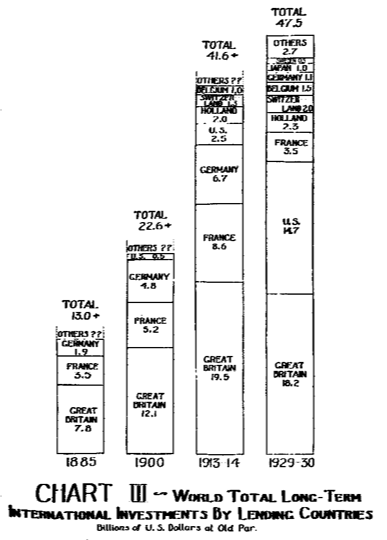

Over time, the accumulation of claims was gigantic. In the years before World War I, according to contemporary sources, the UK accumulated just short of half of all international foreign claims. After World War I the US rapidly caught up, but it was Britain’s huge pile of foreign claims that enabled it to fight both World War I and World War II without financial ruin. As one can see from the Bank of England graph, for much of World War I the UK was still exporting capital to its allies. In World War II the British dipped deeply “into the red”, in the form of Lend-Lease. But that was a short burst of borrowing.

Source: Eugene Staley, War and the Private Investor

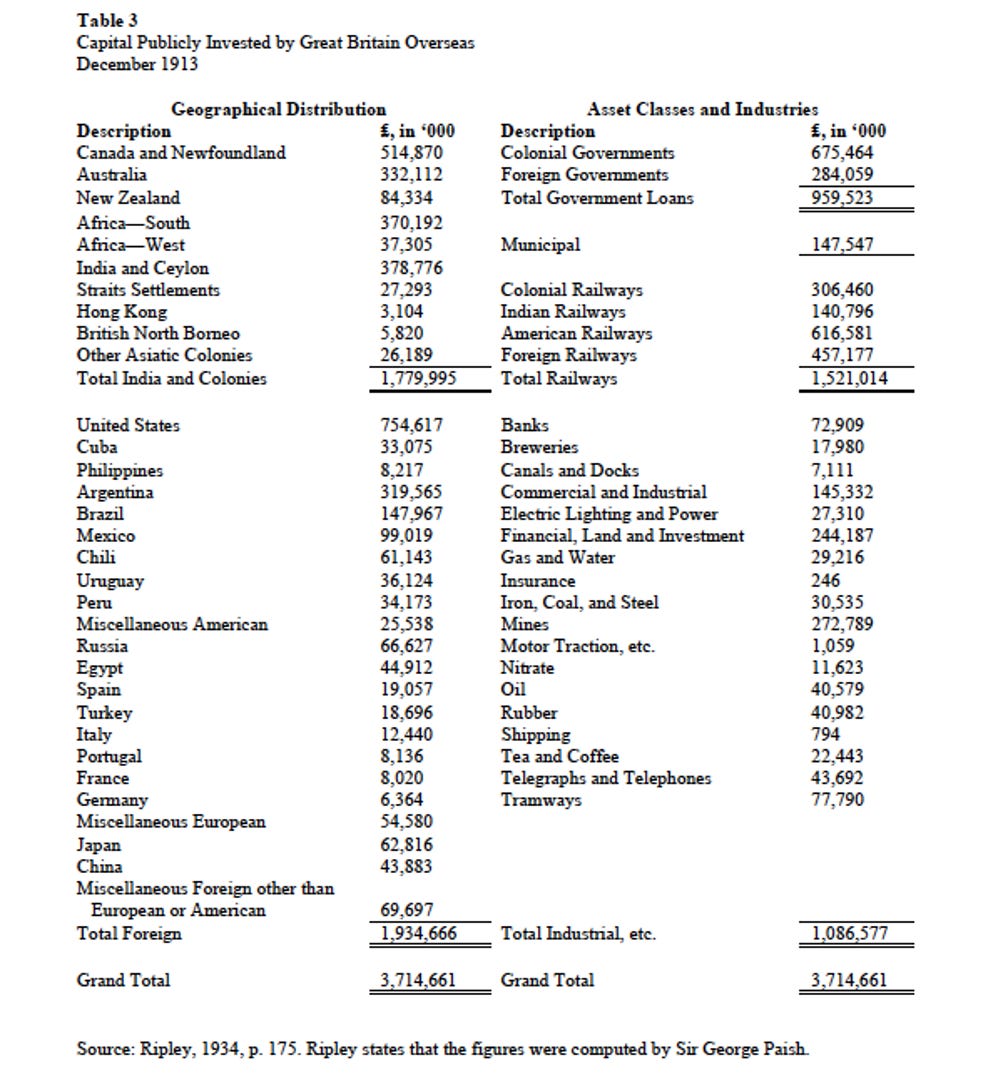

Though there was a substantial imperial component to British overseas investment, the majority of money flowing out of the City of London went to parts of the world that were not British colonies or imperial possessions, first and foremost to the United States. A huge share went directly into infrastructure in the form of railways – one sixth of the giant portfolio was in US railways.

Source: Goetzmann and Ukov (2005)

One can see from the data why Hobson focused on the Boer war. In 1913 Britain had almost as much invested in South Africa as it did in all of its sprawling South Asian possessions. It was British investment that financed the Mexican oil industry. And it was also British money that paid for the world’s largest cattle ranch, the XIT cattle ranch, in Texas. As one Texas historian writes:

British investors helped to introduce barbed- wire fences, steel windmills, deep wells, and better breeds of cattle into Northwest Texas, experimented with various crops, hired Texas “cattle bosses” for a few thousand dollars a year and Texas “cowboys” for twenty-five to thirty dollars a month, paid such taxes as they could not avoid, supplemented the income of some state officials and more lobbyists, and finally, in desperation, made considerable effort to attract settlers …

Yup! Wind power in gilded-age Texas, courtesy of the City of London.

Source: Texas coop power

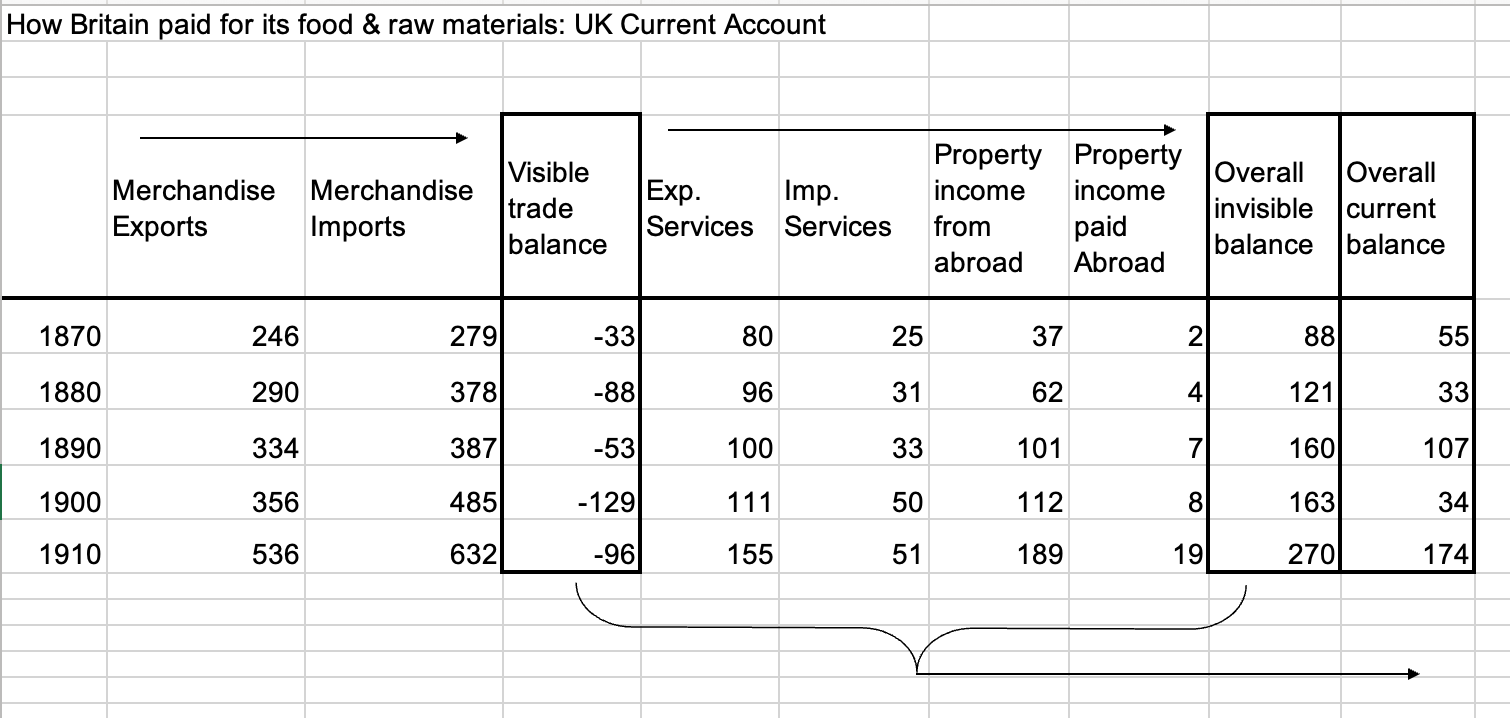

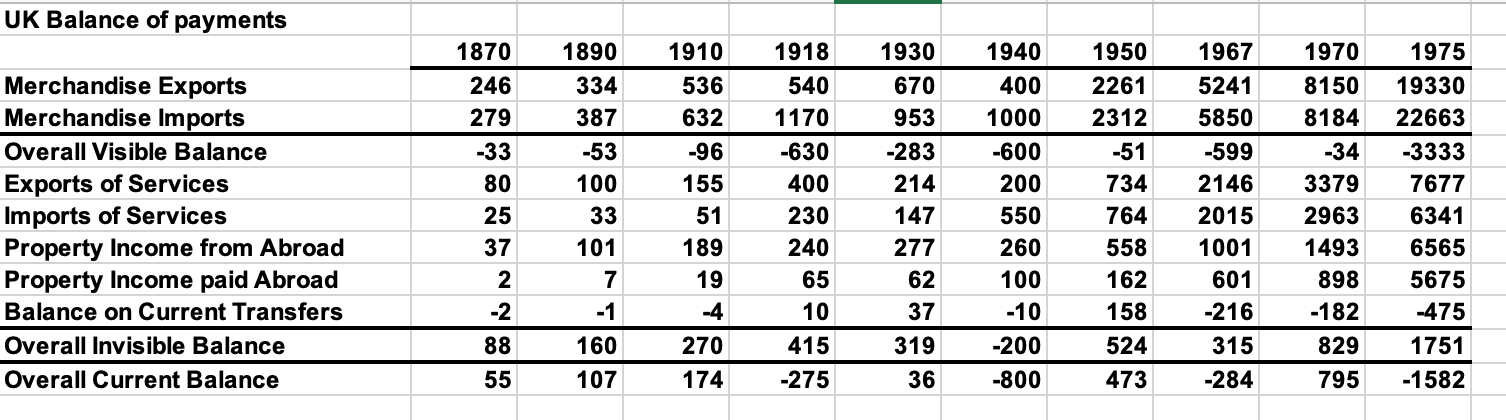

To sustain this giant net outflow the UK ran a current account surplus. But the composition of that surplus is interesting. What it shows is that analogies to the contemporary USA are superficial. In macroeconomic terms, at least, Edwardian Britain was not in the buiness of “imperial tribute”. It was a hard-working hegemon.

From the Victorian period onwards, the UK, like the US today, ran a trade deficit. It provided markets for foreign competitors, triggering an unceasing debate about national decline and elites selling out “British industry”. Hobson was part of that debate about British decline, creating another subtext of confusion when he is invoked in 21st century America. Because, unlike in the US today, British goods exports remained robust and diversified, paying for the vast majority of goods imports. Furthermore the trade deficit was more than made up by the large surplus on service income and the even larger surplus from property income from abroad. Overall this generated a large current account surplus that was then reinvested, further increasing the net surplus on property income from abroad. In many years Victorian and Edwardian Britain’s surplus on property income was larger than the overall current balance, meaning that new investment abroad was more than paid for by the proceeds of existing investment. In effect, the foreign investment account was operating like a self-renewing wealth endowment.

From the point of view of hegemonic stability it is hard to think of a better mix: a consistent and large “downhill” flow of capital, widely spread across the periphery of the world economy, heavily invested in developmental infrastructure and sovereign debt, with a wide open trade account that allowed borrowers to repay their debts with trade surpluses. All the while, Britain retained a large and growing export trade whilst shifting steadily into high-value services.

For all the inequality that it rested on, and for all the jealousy it may have engendered, this is the beau idéal of liberal globalization. As far as the British working class was concerned, the gap to the Edwardian elite may have been huge, but there was also an appreciable gap between the “labour aristocracy” of Britain and their counterparts in Europe. Clearly, naked imperial exploitation contributed in some part to this advantage, in India and African colonies notably. But the larger part of the surplus was generated not by direct extraction but by the ordinary operation of global capitalism. Profitable investments in North America, Latin America and Australia generated handsome yields and a further payoff in terms of cheap consumer goods, notably imported food that supported the standard of living of the British working-class.

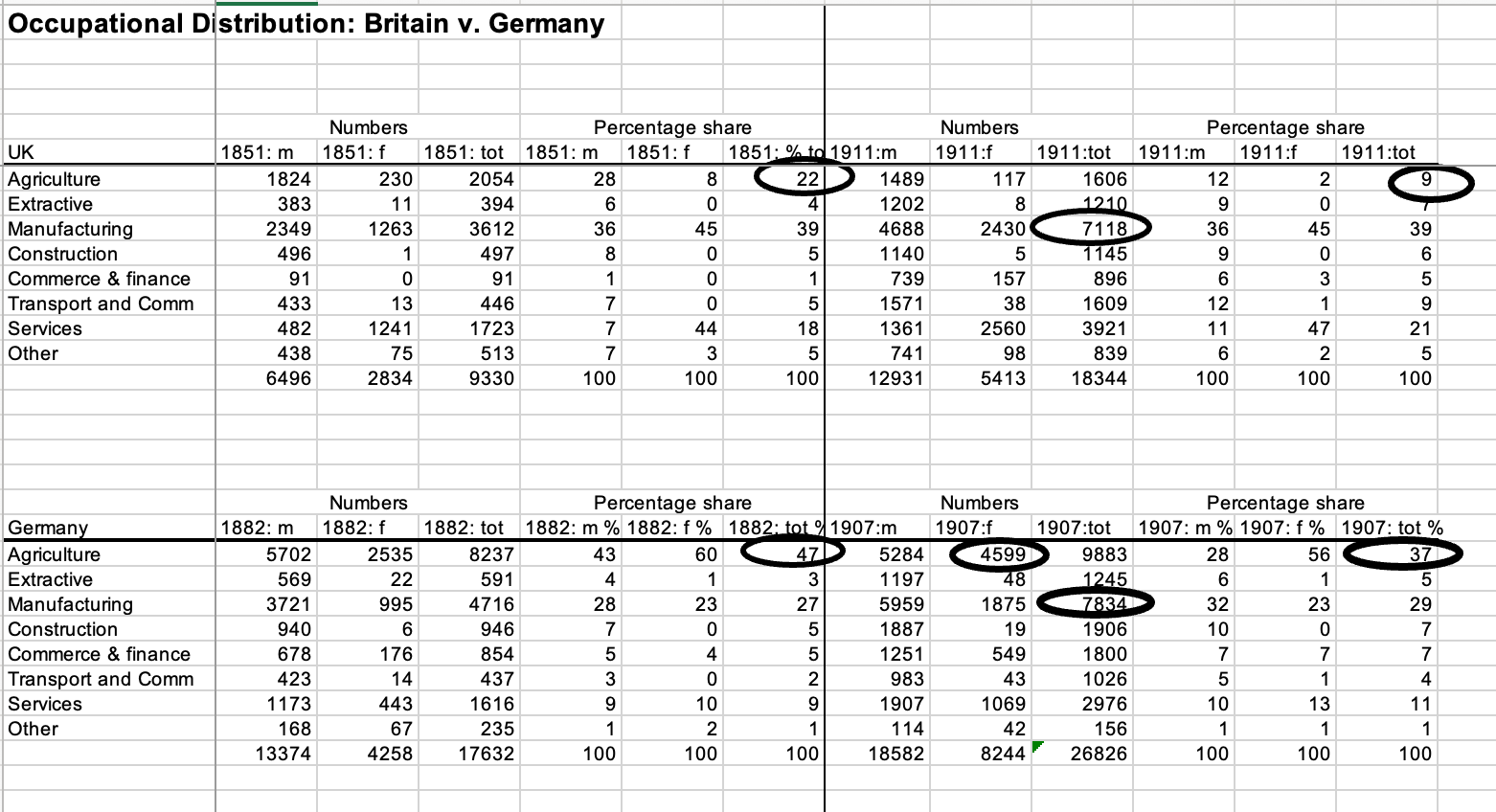

Of course this engendered structural change in Britain, but the biggest difference to comparable European economies, Germany for example, was not the supposed relative decline of British manufacturing (a hotly debated topic in British economic history) but the end of inefficient small-holding agriculture. By 1911 there were few if any “peasants” in the United Kingdom, other than in Ireland, where, for political purposes, London was pursuing a strategy of “peasantization”.

Source: Census for Imperial Germany and the UK

For the song and dance version of this Edwardian ideal type – filtered by way of postwar Hollywood – see Mary Poppins.

The liberal globalization model of the early 20th century did not last. Why not?

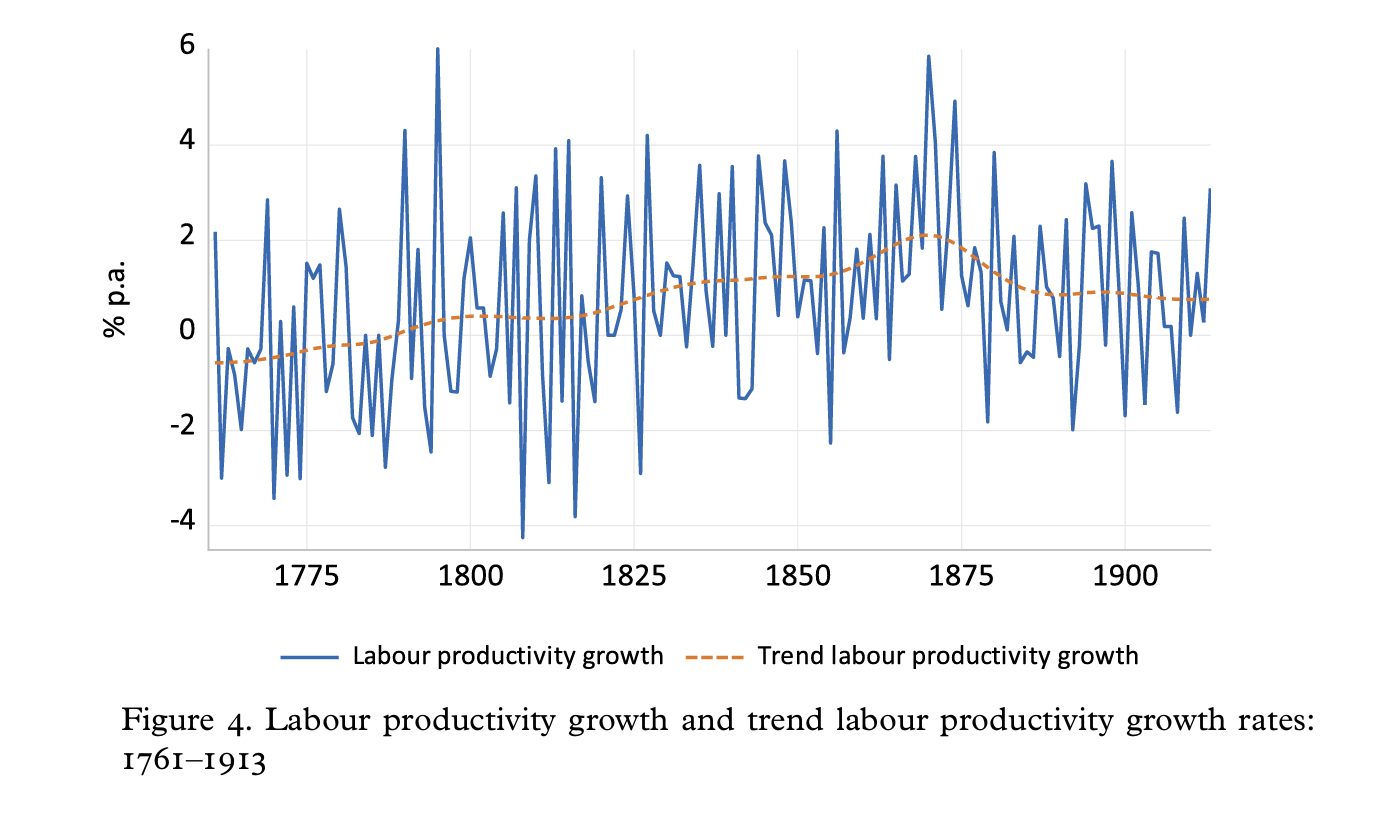

One explanation is a parochial British one. Obsessed as they were with “relative decline”, generations of British economists debated whether high foreign investment, crimped domestic investment and, if so, whether the deceleration was driven by elite anti-industrial bias (yup the Brits got there first on that too), or by inadequate domestic consumer demand (the Hobson underconsumptionist line). The frame of the argument was provided by the “overtaking” of the US and Germany (a thesis stereotypically illustrated by Alfred Chandler in Scale and Scope) and by the more technical empirical finding from the then available GDP numbers (Feinstein’s data were key), which appeared to show that around 1900, Britain experienced decelerating growth – the so-called “Edwardian climacteric” thesis. This narrative has not withstood the latest generation of empirical economic history. Newly revised data for Britain’s GDP, labour productivity and TFP show a relatively steady increase in productivity growth across the industrial revolution from the 1770s to the 1870s; an upward “blip” and a downward “shock” around 1873; followed by stabilization on a high plateau of steady productivity growth by historical standards.

Crafts, Nicholas, and Terence C. Mills. “Sooner than you think: the Pre-1914 UK Productivity Slowdown was Victorian not Edwardian.” European Review of Economic History 24.4 (2020): 736-748.

A less parochial set of explanations for the collapse of gilded age globalization, is offered by neo-Polanyian economic historians, who argue that the very success of globalization in restructuring the world economy produced a backlash from those group who lost out in the distributional struggle. Workers in countries receiving mass migration espoused nativism and immigration restriction. Producers in economies whose markets were flooded with imports turned protectionist. Anyone with heavy debts had reason to oppose the gold standard, which provided the financial frame for the regime. This is what Karl Polanyi, in the Great Transformation (1944), called the “double movement”. One can thus offer a counterfactual history in which globalization collapses in the early 20th century under the weight of its own success. whatever happens in 1914. Britain was not to the fore in the waves of protectionism and nativism that swept the world in the 1870s and 1890s. But it got there in the end. As David Edgerton and Martin Daunton have shown, in the 20th century Britain too would move towards imperial preference and then towards the construction of a national economy.

But the more immediate trigger for the downfall of British-financed globalization were not endogenous economic forces, or “neo-Polanyian” political economy, but the explosion of imperialist competition in World War I and then again in World War II. Whether or not you wish to regard the wars themselves as endogenously, economically induced, is a debate for another time. My own money, as I’ve set out here, is squarely on a Gilpin-style model of hegemonic war. World War I was not principally the result of competition between rival imperialist investors, but of more basic processes of uneven and combined development within Europe, notably focused on the balance between the fragile Ottoman, Habsburg and Tsarist empires with Germany as a lethal accessory, thus widening the war to a global struggle between the European powers.

In any case, it was the wars, not productivity differentials or protectionist backlash that undid the UK’s fortress balance sheet. In the interwar period, Britain’s handsome current account surplus was under threat. World War II was a second financial disaster. In the postwar period, the UK was forced, on occasion, to run a trade surplus, a previously unheard-of situation.

In short, however useful the general Hobsonian analytic of inequality and aggregate demand may be for thinking about our contemporary world, we should not be under any illusion that the situation Hobson was criticizing has much structurally in common with the world of the 21st century. In its most fundamental features, the world economy before 1914 conformed to classical economics – capital flowed “downhill” from capital-rich to capital-poor regions. The world of the 21st century and the structure of American power today is much stranger than that.

I love writing the newsletter. If you enjoy it too and fancy buying me a coffee once a month, you know what to do. Click below!

{kind=link}