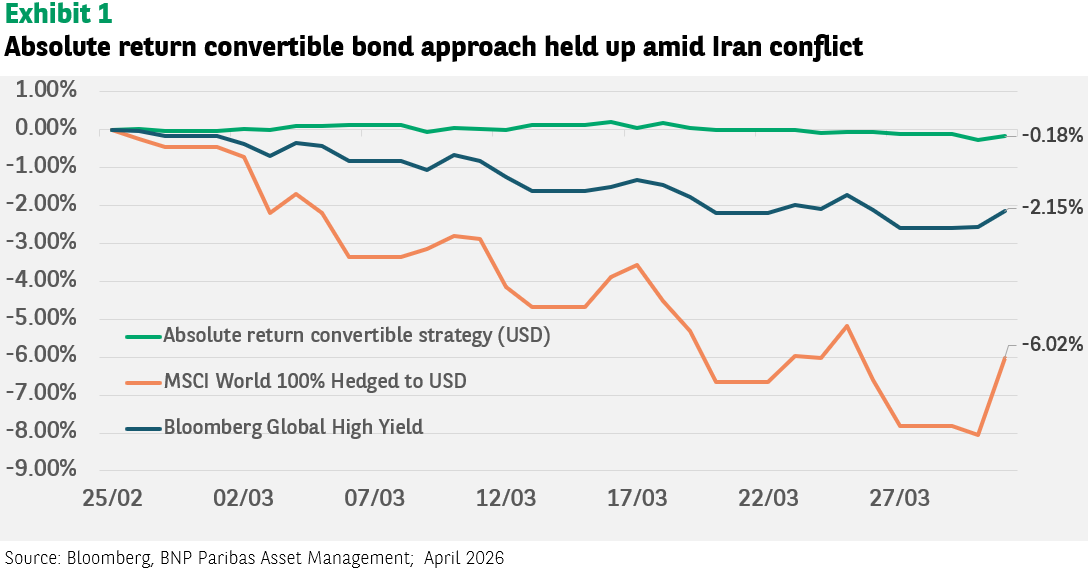

Applying an absolute return approach to investing in convertible bonds has historically provided steady returns for investors across various market cycle: returns remained resilient during, for example, the COVID pandemic and the Ukraine war. Even now, with the Iran conflict, this approach has continued to be a safe heaven.

In this article, Skander Chabbi, Pierre Tuccella, and Sebastien Taldir examine this strategy, clarifying how it generates returns, provides overall diversification and why it’s relevant in the current context.

Absolute return in convertible bond investments

Absolutes return convertible bond strategies are designed to deliver stable returns, achieve a consistent market decorrelation, and maintain low volatility.

We will focus on two complementary strategies – convertible bond (CB) arbitrage and carry strategies. They can both serve as the foundation for an absolute return convertible bond approach.

CB arbitrage exploits mispricing between a convertible bond and its underlying components. As a hybrid security, a convertible bond combines a traditional bond and an embedded option that allows the holder to convert the bond into shares of the issuing company. Financially, it can be viewed as a straight bond plus a call option on the equity.

The classic CB arbitrage strategy consists of buying the convertible bond while shorting the underlying stock in a proportion that neutralises equity market risk (known as delta1 hedging). The objective is not to take a directional view on the share price, but to isolate other sources of return, notably volatility and relative value.

From a volatility standpoint, the investor is typically long gamma2 and vega3 through the option component. By dynamically rebalancing the equity hedge, profits can be generated if realised volatility exceeds the volatility implied in the convertible bond’s price.

This allows returns to be driven primarily by relative mispricing in volatility and/or credit, meaning that returns are decorrelated from equity markets which makes the strategy a useful tool for portfolio diversification.

While historically attractive, CB arbitrage is not risk-free. Liquidity constraints, funding stress, and credit shocks can impair performance, making disciplined risk management essential.

Carry strategies are designed to capitalise on income-focused opportunities

Some convertible bonds offer attractive yields, good credit quality, relatively short duration (less than 1 year) and a low delta1 (below 0.2). Selecting these securities may facilitate consistent income generation while keeping risk low.

Both strategies aim to profit from pricing inefficiencies while keeping equity market sensitivity to close to 0.

A growing demand for CB arbitrage funds

Convertible bond arbitrage, which often is considered a ‘niche’ approach, is well-known in the US and according to the latest Bank of America Global Convertibles Investor Survey, the strategy is becoming increasingly popular in the US and around the world.

Demand for convertible bond arbitrage is strengthening as investors seek strategies that can monetise market volatility while limiting directional risk in increasingly volatile credit and equity markets.

According to the BofA survey, 42% of respondents identify CB arbitrage as the most attractive strategy (see Exhibit 2), making it the clear top choice across the asset class and marking the fourth consecutive quarter it has led investor preferences.

Hedge funds are the primary drivers of this surge in demand. Survey respondents estimate that hedge funds now own over 50% of the global CB market, rising to around 64% in the US, reflecting both capital inflows and the strategy’s scalability.

A still favourable environment for the strategy

The appeal lies in a supportive technical backdrop: single‑stock volatility remains well bid, while primary market activity continues to feed the arbitrage pipeline.

Investors expect nearly $170bn of global convertible bond issuance over the next 12 months, with $110bn from the US and $30bn from Asia, providing ample raw material for arbitrage deployment. Here are some details:

- New supply in January and February ran well above historical averages, defying typical seasonal softness.

- Deals were strongly oversubscribed and delivered solid post-pricing performance, contributing positively not only to outright returns, but also to arbitrage strategies.

- Issuance was largely capital expenditure-driven, particularly linked to AI, datacentres and industrial investment.

- Despite market turmoil in March, new issue volume has remained resilient: $16.1bn came to market (about 1.7x of what’s typical for March), Year-to-date, the global market has priced $53.3bn, more than double 2025’s pace.

At the same time, concerns around stretched valuations — particularly in AI‑linked convertibles, are reinforcing an investor preference for relative‑value strategies over outright exposure.

In this environment, we believe, convertible bond arbitrage stands out as a way to capture convexity4 and issuance premiums while hedging equity risk, helping to explain why investor conviction behind the strategy has been at near record levels.

[1] Delta measures the sensitivity of the option embedded in the convertible bond to the underlying equity price

[2] Gamma measures the rate of change of the delta of the option with respect to a move in the underlying asset. Specifically, the gamma of an option shows by how much the delta of an option would increase by when the underlying moves by $1

[3] Vega measures by how much the convertible price changes when volatility moves by 1%. Higher vega convertibles are more sensitive to changes in volatility than a lower vega convertibles

[4] Convexity measures the sensitivity of the duration of a bond as yields change. This measure assesses the impact on bond prices when there are large fluctuations in interest rates.

{kind=link}