The recent narrative around Malawi’s improving foreign exchange position is rapidly colliding with a harsher reality, raising serious questions about whether the public was given a complete picture.

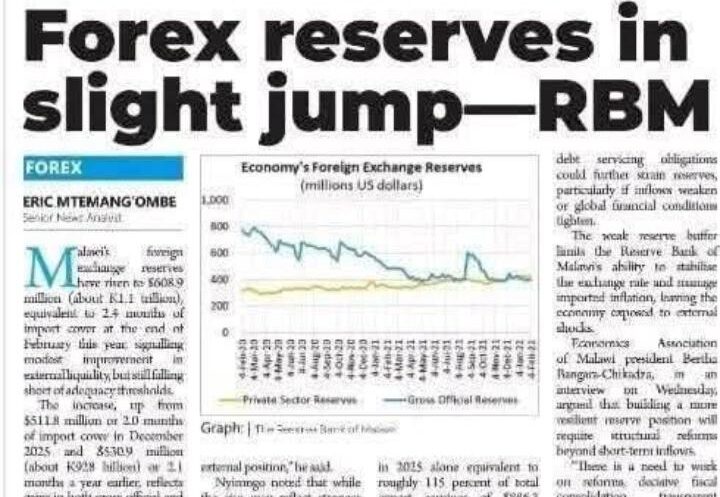

On April 2, the Reserve Bank of Malawi struck an optimistic tone, pointing to a rise in the country’s forex reserves. The figures appeared encouraging: reserves increasing to $608.9 million (about K1.1 trillion) by the end of February, equivalent to 2.4 months of import cover, up from $511.8 million (2.0 months) in December 2025 and $530.9 million (about K928 billion or 2.1 months) a year earlier.

On the surface, this suggested steady improvement.

Yet that sense of progress now looks increasingly fragile. Malawi remains below the widely accepted minimum threshold of three months of import cover for import-dependent economies, and more critically, events on the ground have already begun to contradict the optimism.

Speaking yesterday, government spokesperson Shadreck Namalomba admitted that the country is facing fuel shortages because it does not have sufficient forex to procure fuel. That single statement cuts through the narrative with stark clarity. A country that cannot finance fuel imports cannot credibly claim a meaningful recovery in its external liquidity position.

The contradiction is difficult to ignore. If reserves had genuinely strengthened in a functional and accessible sense, essential imports like fuel would not be under threat. Fuel is not optional; it underpins transport, agriculture, and industry. Its shortage signals not a marginal strain but a deeper imbalance.

This raises the possibility that the headline reserve figure of $608.9 million may not reflect funds that are readily available for immediate use. Portions of these reserves may be tied to debt servicing obligations, held in less liquid instruments, or otherwise committed, leaving the usable forex position significantly weaker than the headline suggests.

Economist Velli Nyirongo had already warned against overinterpreting the increase, describing it as “a cautiously positive development” that does not yet signal sustained improvement. He pointed out that such gains are likely driven by short-term or cyclical factors such as donor inflows, temporary export earnings, or tighter import controls rather than structural changes in the economy. Without consistent growth in diversified export earnings, the country’s forex position remains vulnerable, and any apparent gains can quickly dissipate.

That vulnerability now appears to be playing out. Demand for forex—driven by fuel imports, external debt obligations, and private sector requirements—seems to have outpaced the modest gains recorded in the reserves. This creates a situation where reserves may rise statistically but fail to deliver real-world stability. The fuel shortage is the clearest possible test of forex strength, and it is one the country is currently failing.

This leaves the Reserve Bank of Malawi facing uncomfortable scrutiny. Did it overstate the significance of the increase, or did it fail to communicate the limitations and composition of those reserves? Presenting gross figures without clarifying how much is liquid and immediately usable risks creating a misleading sense of security. When such optimism is followed almost immediately by a crisis as visible as fuel shortages, it erodes confidence in official economic messaging.

Ultimately, the issue goes beyond communication. Malawi’s forex challenges are deeply structural, rooted in a narrow export base, heavy reliance on imports, and dependence on external inflows. Until the country can consistently generate foreign exchange through diversified and competitive exports, any improvement in reserves will remain fragile and short-lived. The rise to $608.9 million is not insignificant, but it is clearly insufficient, and more importantly, it is not translating into the stability that Malawians were led to believe was taking hold.

What remains is a widening gap between official assurances and lived reality. If reserves had truly “jumped” in a meaningful and usable way, the country would not be struggling to secure fuel. That reality, now confirmed by Shadreck Namalomba himself, casts serious doubt on the earlier narrative and forces a difficult but necessary question: were Malawians given the full truth, or just the most comforting version of it?

Follow and Subscribe Nyasa TV :

{kind=link}